In my last post, I focused on the dynamic nature of lithium reserves and resources and the fact that as demand for lithium shoots up, the demand side shouts out to the supply-side to get its act together through the price mechanism. Accordingly, there is no fixed cake of lithium. We don’t just eat one fixed lithium cake in front of us until it has all gone.

The authoritative United States Geological Survey in its latest round-up of the world’s metals and minerals says we have 53 million tonnes of lithium resources available to be exploited as of 2017, compared with 13 million tonnes in 2005. As the table below shows, however, recorded resources do not include unconventional sources, sources that are too low grade (not concentrated enough) or undiscovered resources. The vast majority of lithium within the earth’s crust is either inaccessible deep below ground, at the bottom of the sea, or far too expensive to extract due to its diffuse nature.

Yet that leaves a bunch of lithium that is perfectly usable but remains undiscovered. How much? Who knows. We can get some sense of what is out there by looking at the annual flow of lithium from ‘undiscovered’ to ‘identified’, and (with my economist’s hat on again) seeing how much money is being expended to help that process along.

If you read each year’s edition of the USGS’ Mineral Commodity Summaries, you do get some sense of annual tends, but the USGS doesn’t look forward into the future. For that, we need to listen to “Deep Throat”s advice to Bob Woodward (played by Robert Redford) in “All the President’s Men”. That advice was “Just, follow the money”.

And it was through “following the money” that it suddenly dawned on me that perhaps Tony Seba’s predictions were not so crazed as I had orginally thought four years ago. Now let us see how much money is going into lithium mining expansion and, even more interestingly, where it is coming from.

But before we start, let me give you a bit of context. In my last post, I referred to the assumption by ‘peak lithium’ advocate William Tahil that one kilowatt hour (kWh)’s worth of EV battery storage required 1.4 kilogram (kg) of lithium carbonate equivalent (LCE). More modern estimates are closer to 1kg per 1kWh, which thankfully makes the maths a bit easier too. New generation EVs with a decent range have around 75kWh-sized batteries. From this, we can calculate that to produce one million good specification EVs you need 75 million kgs of LCE, or 75,000 tonnes. Also, keep that lithium carbonate equivalent (LCE) abbreviation in mind, we are going to use it a lot!

The Big Three (SQM, Albermarle and FMC)

Perhaps, we can divide our time line between the ‘Electric Vehicle Era” (EVE) and the “Before Electric Vehicle Era’ (BEVE). Once upon a time in the BEVE there lived three happy oligarchical lithium producers who carved up the market amongst themselves. Because they had access to a relatively cheap source of lithium extracted from brine lakes, no other entrant could enter the market without making a loss.

What is brine in this context? Water with super concentrated amounts of minerals that can include lithium. Due to its higher density, it sinks to the bottom of ordinary bodies of water. The Big Three operators have their core base in the lithium triangle of Chile-Argentina-Bolivia. They pump brine out into evaporation pools and then let the sun remove the water, leaving a mineral sludge. And for your added edification, here is a video of an eel having an unfortunate encounter with a deep sea brine lake as narrated by David Attenborough in Blue Planet 2:

And for a seriously sized evaporation pond, look at this one belonging to SQM:

Sociedad Química y Minera de Chile (SQM)

One of the biggest of the oligarchs is SQM, which in 2017 had revenues of $2.2 billion, a third of which come from lithium. The company’s web site is here. The company has a somewhat murky pedigree, with the son-in-law of former strongman and ruler of Chile General Pinochet being a key shareholder.

The company is allowed by the government of Chile to extract 350,000 tonnes of lithium metal from one of the largest brine lakes in the world called the Salar de Atacama. This lithium budget is good until 2030 under an agreement reached in January 2018 following a very fractious round of negotiations. Chilean lithium companies have to broker agreements with CORFO, the Chilean government entity that licenses extraction rights to Chile’s lithium resources in exchange for royalties. The new deal translates into 2.2 million tonnes of lithium carbonate equivalent (LCE, see my last post for an explanation of contained lithium metal and lithium carbonate equivalent).

In 2017, SQM produced 48,000 tonnes of lithium carbonate and 6,000 tonnes of lithium hydroxide, which amounted to 23% of world supply according to them.

Under the agreement with CORFO, these numbers will rise to 100,000 and 13,500, respectively over the next two years, and could in aggregate rise again to 180,000 per annum while staying within the extraction budget set by CORFO through to 2030. Simplistically, that equates to about 2.5 million decent specification EVs worth of lithium, assuming that SQM suddenly stopped supplying lithium for any other end use. In reality battery quality LCE needs a certain level of purity that other applications don’t necessarily need. But we will keep hold of this quick and dirty equivalence; that is, 75,000 tonnes of LCE equates to one million EVs.

SQM also have a number of joint ventures in other countries, but they are not yet at the stage of producing lithium. We will come back to that.

Albemarle

The US-stock market listed Albemarle (web site here) is also active in Chile with operations at the same brine lake as SQM, the massive Salar de Atacama. In addition, it has a much smaller brine operation in Clayon Valley, USA, together with a bigger hard rock joint venture at Greenbushes Australia (49% Albemarle, 51% Tianqi Lithium of China). In 2017, the company produced 65,000 tonnes of LCE, which it plans to raise to 165,000 in 2021 and 265,000 sometime thereafter.

The company has considerable downstream processing capabilities, added to after purchasing Jianxi Jiangli New Material in 2016. As a reminder, lithium brines and lithium ores (spodumene) are at the top of the lithium supply chain, and from these feedstocks various processing stages take place in order to obtain a variety of useful lithium-based products. For battery production, the most important of such intermediate materials are lithium carbonate and lithium hydroxide. An Albemarle slides gives you a sense of the complexity:

With so much lithium in Chile being produced by SQM and Albemarle, battery component and module makers have been drawn to the country like a dog to a pool of sick.

The Chilean government has a development strategy based around capturing more of the lithium value chain in-country by, in effect, guaranteeing supply to only those processing companies that promise to set up lithium plants in Chile. So far, COMFO has indicated that 25% of Chile’s production (basically 25% of SQM and Albemarle‘s Chile production) will be preferentially allocated to Chilean-based processing plants.

Currently, the following companies are proposing in-country operations in exchange for guaranteed lithium supply:

- TVEL Fuel Company of Rosatom of Russia.

- Suchuam Fulin Industrial Group Co. Ltd of China.

- Shenzheng Matel Tech. Co. Ltd. and Jiangmen Kanhoo Industry Co. Ltd. of China.

- Molymet from Chile.

- Gansu Daxiang Energy Thecnology Co. Ltd. of China.

- SAMSUNG SDI Co. Ltd. and POSCO of Korea.

So we can see a host of battery component makers desperate to nail down their lithium supply, and they are happy to spend a lot of money setting up processing plants in Chile to achieve such an aim.

FMC

FMC (web site here) started out in life as the US-goverment founded Lithium Corporation of America, which was purchased by the New York Stock Exchange-listed FMC in the late 1980s. In 2017, the company produced 18,500 tonnes of LCE from its brine operations based in Argentina at the wonderful sounding Salar del Hombre Muerto. It aims to raise output to 21,000 tonnes in 2018, 31,000 tonnes in 2020 and 41,000 tonnes in 2022.

FMC has a wide range of chemical business and lithium only makes up less than 10% of revenue. Since lithium is viewed as a growth area, the company intends to spin out its lithium segment in an IPO in the autumn of 2018 as it believes a separate listing will get a premium stock market valuation.

Big Three Signal Capital Intentions

LCE production in 2017 was around 215,000 tonnes according to FMC. From the company presentations of the Big Three, we can therefore work out market shares.

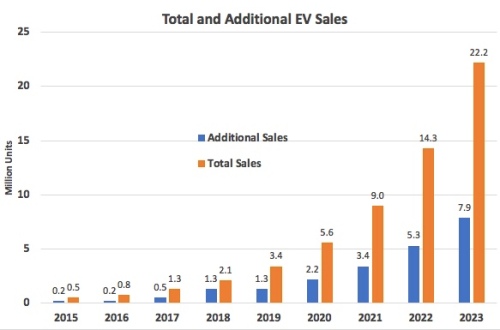

From the expansion plans published by the Big Three, we also know that they intend to increase LCE production from 125,000 tonnes in 2017 to 485,000 tonnes sometime after the year 2022. That is almost a fourfold increase. If we take that growth rate and apply it to the entire world, we should expect to see global LCE production of around 825,000 tonnes in and around 2023. That is a useful date, as it allows me to recycle this chart, which I haven’t done for a while:

At the top of the post, I said my ranging shot for LCE to EVs was this equality: 1 million EVs = 75,000 tonnes of LCE. My lithium production extrapolation above has us producing 825,000 tonnes of LCE around 2023. This amount of lithium could outfit about 11 million EVs in 2023: not enough for us to keep on Tony’s S curve. Of course, this assumes that the entire global lithium supply is dedicated to EVs (no more iPhones).

Therefore, the numbers don’t add up. To get them to match we need to alter things around. We have four choices: 1) don’t make so many EVs, 2) change the size of the batteries, 3) use less lithium by changing battery chemistry or 3) mine more lithium.

Let’s take a slide out of FMC‘s presentation to the Barclays Electronics Chemicals Conference May 14, 2018 (find the presentation here):

There are a lot of interesting things we can pull out from this. First, the most bullish broker has 938,000 tonnes of LCE being produced in 2025. That would be in line with my extrapolation. Second, there is a general consensus that average battery size will be 50kWh. If true, that gives us 50% more EVs per million tonnes of lithium than I had, getting my ranging shot estimate of EV sales numbers up to 16 million. That is close to where we need to be on Tony Seba’s S curve. Moreover, that same broker is only using 0.7kg of LCE per kWh. I think that is too ambitious, but we will come back to that when we delve more into battery chemistry.

Overall, the supply response from the lithium miners looks pretty good from the chart above. But is it good enough? At the beginning of the post I invited you to “follow the money”. We can see the Big Three intend to quadruple production over the next few years and that takes a lot of money. But the Big Three are doing the investment internally. To really see the tidal wave of new money coming into the sector you need to look outside of the Big Three. Moreover, for me, this wave of money suggests we could get to well above 1 million tonnes of LCE by the year 2025. That will be the subject of my next post.

For those of you coming to this series of posts midway, here is a link to the beginning of the series.