Following on from my 20-post series on elective vehicle (EV) penetration rates (which started here), I’ve been mulling a series of posts on the Tony Seba’s forecasts for solar energy growth through to 2030.

Just as with EVs, I am less interested in proving Seba right or wrong; rather, I am using his forecasts as a hook to examine the question of whether such warp-speed technological revolutions are possible. If Tony is right, or even half right, such a disruption will upturn all of our current socio-economic arrangements. In short, the transformation will re-order the wealth of nations, change how our cities and towns are arranged and upturn how we work and play.

Tony Seba is frequently attacked by industry insiders as a publicity-seeking charlatan, with dubious academic credentials and limited knowledge of the fields he opines on. Perhaps. But you can’t accuse of him of refusing to present testable hypotheses, the litmus test that divides evidence-based science and irrefutable faith. In Tony Seba’s 2014 book “Clean Disruption“, we find this passage on page 37:

Globally, solar PV installed capacity has grown from just 1.4 GW in 2000 to 141 GW in 2013. This represents a compounded annual growth rate (CAGR) of 43 percent.

Should solar continue to grow at a 43-percent annual clip, the solar installed capacity will be 56.7 TW by 2030. This is approximately the equivalent of 18.9 TW of conventional caseload power. World demand for energy is expected to be 16.9 TW by 2030, according to the US Energy Information Agency.

Should solar continue on its exponential trajectory, the energy infrastructure will be 100-percent solar by 2030

The use of the word “should’ isn’t his ‘get-out-of-gaol-free’ card since he continues later in the book to suggest that installed capacity growth will grow faster than 43% per annum.

If you want to hear Tony’s claims directly, then listen to this presentation from 50 minutes into the talk:

Solar, the installed base, has doubled every two years since the year 2000. This is on a global basis. That is, basically, a growth compounded at 40% per year. Doubled every two years since the year 2000. Now, solar is about one and a half per cent of generation…..

…..Now if it keeps doubling, and it keeps doubling every two years, how long, how many years, until solar is 100% of the world’s generation of energy ? Let’s do the numbers. So one and half percent, let’s double it every two years. Three percent, one doubling, six, 12 percent, 24, 48, 96. Six doublings. Say I am wrong by a couple of years. Seven doubling, that is 14 years, so essentially by 2030 or so, solar, if it keeps growing like this, and remember S-curves, right, exponential. It’s going to be 100% of the world’s energy generation.

Tony then goes into the respective cost curves of solar versus incumbent energy sources (which I will address in later posts).

OK, let’s put this up against competing forecasts from more mainstream institutions, starting with the International Energy Agency (IEA). This chart from their World Energy Outlook 2018:

In the above chart, NPS stands for New Policies Scenario and SDS the lower carbon Sustainable Development Scenario. Regardless, renewables don’t get much above 25% at best and that is full ten years after Tony’s projected solar-dominance date, plus the renewable category includes all renewables and not just solar.

Let’s look at a few more flagship publications that deal with long-term energy forecasts. In the US, the government’s Energy Information Administration (EIA) puts out an publication titled Annual Energy Outlook that goes out to 2050 as well. It’s US centric, but since so much technology and finance comes out of the US, one would expect the country to not be far off the global solar adoption pace.

For the EIA‘s 2018 edition, solar sits in the “other renewables” category (which excludes hydro). We will disaggregate the other renewables category in later posts, but suffice as to say if solar were doubling every two years, the green curves should be standing up. Instead, the EIA has growth slowing down.

A number of the oil majors also put out long-term energy forecasts. From BP’s Energy Outlook 2018. They have a variety of scenarios, the most aggressive for renewables is called “RE push”. That scenario has all renewables accounting for around 20-25% of energy consumption by 2040.

And from Exxon’s 2018 Outlook for Energy. Wind and solar barely show up:

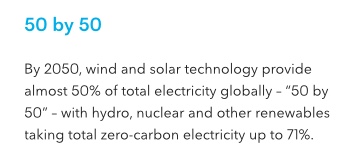

Finally, a friend of green energy, Bloomberg New Energy Finance makes this forecast in its New Energy Outlook 2018:

So that is all renewables accounting for only 50% of electricity production, rather than 50% of total energy production or consumption, by 2050.

The main takeaway from this introduction is that Tony Seba’s solar penetration forecasts appear even more aggressive, and even more non-consensus, than his EV sales forecasts. Are they completely barking mad?

To be continued…..