Yesterday, I was a grump over national competitiveness and, in particular, the World Economic Forum‘s Global Competitiveness Index. I remain a grump today. Why does this topic bring out the curmudgeon in me?

In short, because national competitiveness is like a shell game where you are shown one definition, and this is then secretly switched to another. Here is a part of a speech by Prime Minister David Cameron on the UK economy in March 2013:

But third, as I said, we are restoring our competitiveness. At the forefront of this is our bold plan to cut corporation tax to 21%. That will be the lowest in the G7. As the recent KPMG survey shows, in just over two years we’ve transformed business perceptions of our corporate tax system from one of the least competitive to one of the most competitive in the world. We’re introducing some of the most generous tax breaks for early investment start-ups of any developed economy on the planet. And, by stripping back the red tape that was smothering businesses, we’ve put Britain back in the World Economic Forum’s Top Ten for competitiveness.

We start with the use of the word ‘competitive’ in the traditional sense: something relative to another. The claim is that UK tax rates are more competitive because they are lower. But this is really a tautology. Put another way, Prime Minister Cameron says this state of affairs is good, because good is defined as being this state of affairs. The only external evidence for the goodness of this state of affairs is the fact that it helps “put Britain back in the World Economic Forum‘s Top Ten for Competitiveness”.

Then later in the speech we see the race metaphor raised:

But my message is simple, people should make no mistake, in this battle for the future of Britain and our competitiveness, I’m prepared to roll-up my sleeves and have a fight, if that’s what it takes. So that is our plan: fiscal responsibility, monetary activism and restoring our competitiveness to succeed in the global race.

And it’s a zero sum race, since if we don’t beat the Chinese and Indians our children won’t get good jobs:

My motives, my beliefs, my passion for sticking to this plan are exactly about doing the right thing to help families and to help businesses up and down our country, because the truth is this: because if we want good jobs for our children, we will not get them if we are burdened with debt and outcompeted by India and China.

And in case you don’t get the message, the speech finishes by battering you with the race metaphor again:

By sticking to the plan, we can together make Britain a great success story in this vital global race. Thank you.

In all, I counted 16 references to ‘competitiveness’ and ‘competing’ in the speech. Productivity: zero. Prosperity: zero. Well-being: Zero.

Quick refresher on the WEF‘s definition of competitiveness, from page 4 of the Global Competitiveness Report 2014 /15:

We define competitiveness as the set of institutions, policies and factors that determine the level of productivity of a country. The level of productivity, in turn, sets the level of prosperity that can be reached by a country.

Note there are no sport or military metaphors to be seen. We neither appear to be in a race or a battle, just striving for a bit more boring productivity.

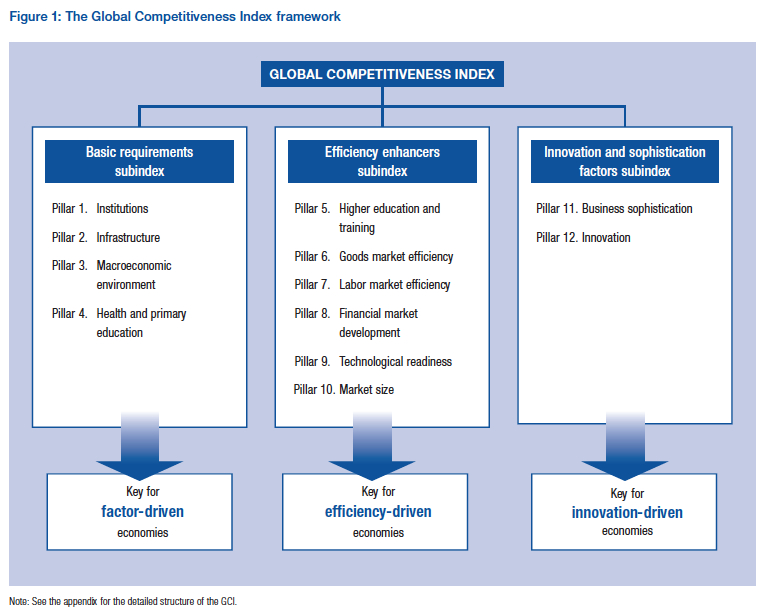

The report then sets out the twelve pillars that make up competitiveness, with these in turn determining productivity. The pillars are as follows:

- Institutions

- Infrastructure

- Macroeconomic environment

- Health and primary education

- Higher education and training

- Goods market efficiency

- Labor market efficiency

- Financial market development

- Technology readiness

- Market size

- Business sophistication

- Innovation

And a pretty chart (click for larger image):

The calculation then gets more complex. Each pillar is subdivided into smaller categories, and each category is given a weight and a score. Moreover, the weightings differ depending on a country’s level of development. The rationale behind the particular weightings for each category is not revealed. Weightings appear to drop into the report like manna from heaven.

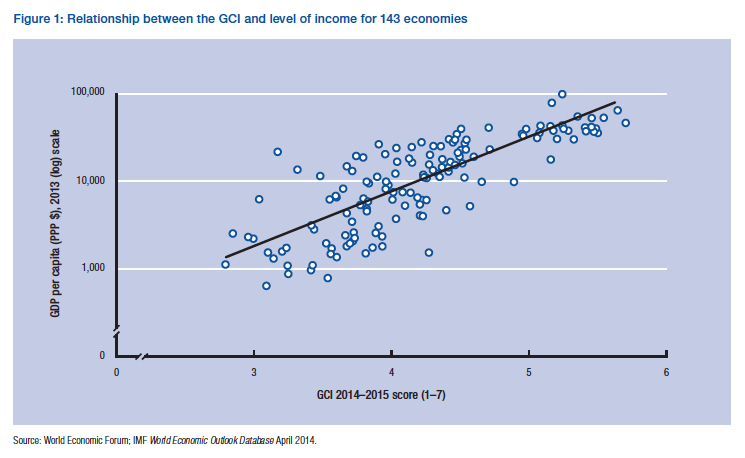

We now get wonkish as we delve into Appendix A titled “Statistically testing the validity of the Global Competitiveness Index as an estimate of the level of productivity of an economy” on page 46 of the report. In this part of the report, we are told that it is too difficult to measure productivity directly so GDP per head is used as a proxy. The following chart is then produced (click for larger image):

Hang on. What does this chart actually tell us? That rich nations have better institutions, education and so on. Do we really need a 500 page report to tell us that? And from statistics 101 we know that correlation doesn’t equal causation. And if there is causation, which way is it going. As we get richer, doesn’t that allow us to have better institutions and get more educated? Moreover, the accompanying text tells us that the GCI score accounts for only about two-thirds of GDP per capita anyway.

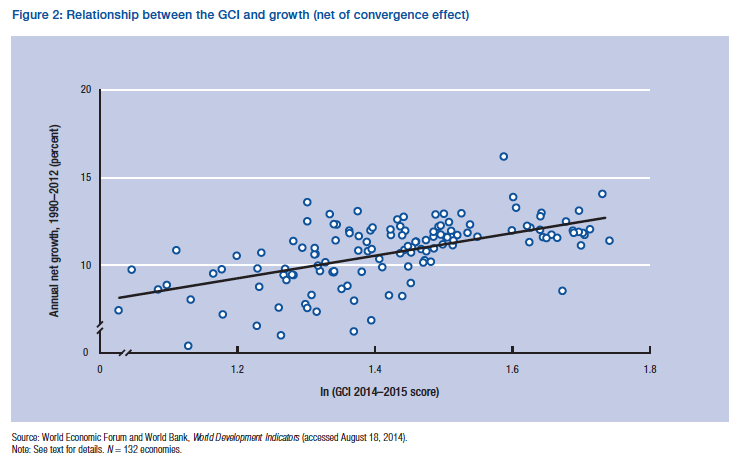

A second chart is then produced to give further credence to the GCI and productivity link. We have a little bit of sleight of hand here because we are jumping from a static to a dynamic measure: from GDP per head over a snapshot in time to GDP growth over a period of time. This is a little bit bizarre. We are saying that productivity should raise the long term growth rate. Yet the long-term growth rate is mostly driven by the change in productivity. So the idea is that if you are productive now, you will be more productive in the future. In short, innovation will continue–probably one of the most inane statements I have ever heard.

Note that in the above chart they have adjusted the growth number to take account of convergence (other things being equal, poor countries grow quicker than rich ones).

The other thing that jumps out at me from this chart (apart from all the correlation/causation problems) is that we are going backwards: the 2014/15 index score is being used as the determinant of growth from 1990-2012. Shouldn’t we really be taking the first GCI scores published in 2004 and then plotting them against the growth rates over the subsequent decade?

Despite all this, the WEF pats itself on the back and says job well done:

In conclusion, the results of both Figures 1 and 2 indicate that the GCI is a good estimate of the level of productivity. In other words, the GCI’s estimate of the determinants of competitiveness–which, in turn, fundamentally shape the (conditional) medium to long-run growth rate of an economy and its level of prosperity–is validated on a statistical level.

Between David Cameron and the WEF, we now appear in a hopeless muddle. The British prime minister bangs on about competitiveness using the metaphor of a global race. As such, Britain should rejoice that it has gone up the WEF’s Global Competitiveness Index league table. But the WEF says that the GCI is a measure of productivity, and since no-one can really measure productivity, it measures GDP per head (and it is a pretty crap measure of GDP per head at that). But if David Cameron goes along to the UK’s Office of National Statistics web page, he can read off Britain’s GDP per head statistics directly. So what is the bloody point of the GCI!

OK, in the final statistical results paragraph I quote above, an allusion is made to the GCI having some forward-looking predictive power. That is, if you raise your score today, you will become richer tomorrow. But where is the evidence in the WEF report to support this assertion? In truth, there is none.

Now within the index, there are a bunch of GCI pillars that if bolstered I am sure would lead to greater prosperity. Who doesn’t like innovation and higher education? But mixed in with this we have lower corporate tax rates, flexible labour markets (code for fewer labour rights), deregulation and privatisation. These factors are submerged within the GCI methodology like ingredients in a giant Irish stew. Do we know if any of these factors has a bearing on future productivity: no, we haven’t a clue.

In conclusion, appealing to competitiveness is often little more than a game of bait and switch, under which one kind of political agenda suddenly morphs into another. Be warned. Grump over.