As I write this post, I am looking out at a Tokyo skyline the day after the most radical ever experiment in Japanese monetary policy was announced. The new central bank governor, Haruhiko Kuroda, has promised to double the monetary base over the course of two years and buy government bonds. And if that doesn’t do the trick of reigniting inflation, then he will buy some more.

In and of itself, doubling the monetary basis is meaningless in terms of GDP unless it translates into an expansion of credit. That is credit to households (allowing greater consumption), to corporations (allowing greater investment) or to government (allowing greater public spending),.

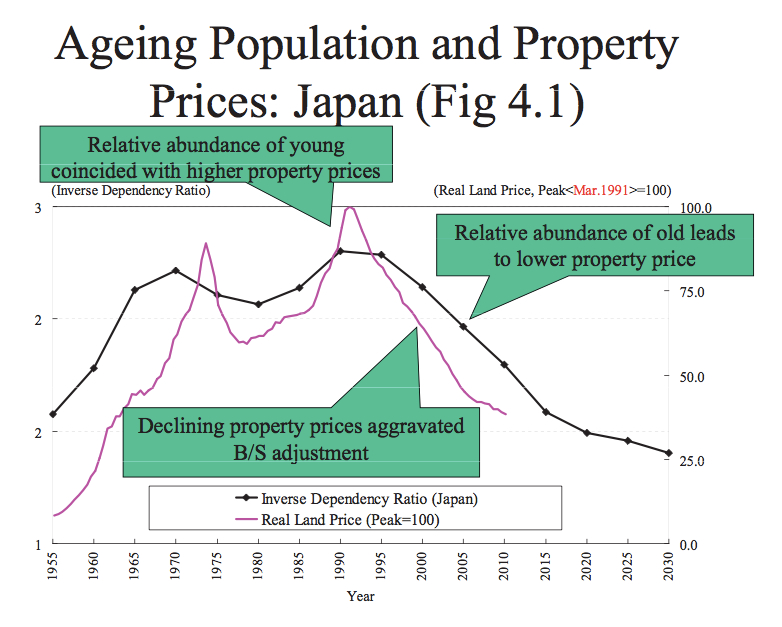

The assumption behind all of this is that Japan’s current rate of economic growth—basically close to zero—is ‘unnatural’. In other words, despite Japan’s ageing demographics, stagnating productivity gains and negative exposure to the long-term upward trend in commodity prices, Kuroda believes that Japan still deserves to grow at 2% per annum or so.

In your dreams.

To be effective, Kuroda’s approach requires a transition mechanism between the monetary economy and the real economy. Given he is buying assets, that transition mechanism rests with the asset markets. But what he ultimately wants to influence is a flow, that is GDP, not a stock, that is asset prices. Putting the government to one side, Kuroda’s game is to crowd out individuals, banks and corporations from the Japanese government bond market. His clearly stated goal is to ignite 2% inflation, but his specific policy tool is to keep interest rates close to zero all along the yield curve to as far out as 40 years. So he is saying loud and clear: “Bugger off out of government bonds or else I’ll inflate you away!”

“Be careful what you wish for,” I mutter to myself.

For a start, he must be careful that they “bugger off” in an orderly fashion. If everyone “buggers off” en masse all at once—and the Japanese do love a craze— Kuroda ends up owning the Japanese bond market. Last week, the Bank of Japan published its latest ‘flow of funds’ comparing Japan with the U.S. and Euroland (click the chart for larger image). As you can see, households, particularly the elderly ones, are clustered in bank deposits. The banks, in turn, invest in Japanese government bonds. So basically the majority of household savings are invested in the equivalent of a Japanese mutual fund for bonds—just at one step removed.

So, to repeat, Kuroda wants them to “bugger off” out of their indirect Japanese bond mutual fund holdings and do something more constructive with their money instead. Paraphrasing Monty Python’s “Life of Brian”, the question then is “How shall we bugger off, O Lord?”

ARTHUR: Hail Messiah!

BRIAN: I’m not the Messiah!

ARTHUR: I say You are, Lord, and I should know. I’ve followed a few.

FOLLOWERS: Hail Messiah!

BRIAN: I’m not the Messiah! Will you please listen? I am not the Messiah, do you understand?! Honestly!

GIRL: Only the true Messiah denies His divinity.

BRIAN: What?! Well, what sort of chance does that give me? All right! I am the Messiah!

FOLLOWERS: He is! He is the Messiah!

BRIAN: Now, fuck off!

silence

ARTHUR: How shall we fuck off, O Lord?

Let’s take an example. Imagine a veteran of the accounts department of stodgy Nippon Life Insurance. He has been handing over his salary to his stay-at-home wife (I will call her Mrs Watanabe for the sake of convention) for decades, who in turn has been socking away Y2 million a year to create a nest egg north of Y100 million, or well over one million U.S. dollars. Kuroda is threatening her with 2% inflation against a deposit that returns close to zero. Now what will she do?

I will tell you what she won’t do. She won’t put her money into an early stage start-up fund. And she will definitely won’t bank roll her waster grandson who works part-time in Seven-Eleven but says he has a great idea for an iPhone app that morphs pictures of Facebook friends into manga porn (which would probably be a good enhancer of GDP).

What she may do is invest in a foreign currency investment trust that the nice sales lady from Daiwa Securities said was a good investment when she visited Mrs Watanabe’s house the other day. She may also invest a bit in some blue chip Japanese equities. And perhaps she will visit Ginza Tanaka, a firm whose hushed halls elevate the sale of physical gold to performance art. Will any of this increase GDP? No.

Then there is real estate. Much as Mrs Watanabe hates her son-in-law, he is already 40 and still rents—which is, well, embarrassing. So we could see some trickle down there, especially since a few tax breaks to encourage such behaviour have recently been announced.

Yet, in aggregate, this kind of behaviour will just translate into a little bit more scrap and build, since Japan’s housing stock is ample to accommodate present and future households. In fact, net household formation has turned negative, as households are being extinguished through death as fast as new ones are being formed. Her son is part of the baby boomer echo generation, which has already fallen out of the child-bearning years; and behind him come a batch of severely depleted cohorts with a lukewarm attitude to marriage and childbirth.

Housing can only drive growth over the long term, if population growth is driving housing—otherwise it won’t. Indeed, residential investment as a percentage of GDP has fallen by almost half in the last 10 years from a little over 5% to just over 2%. You can see this key driver of the housing market in a chart taken from a BOJ presentation (here):

Looking at all the above, will rising real estate prices help enhance Japan’s long-term potential growth rate. No.

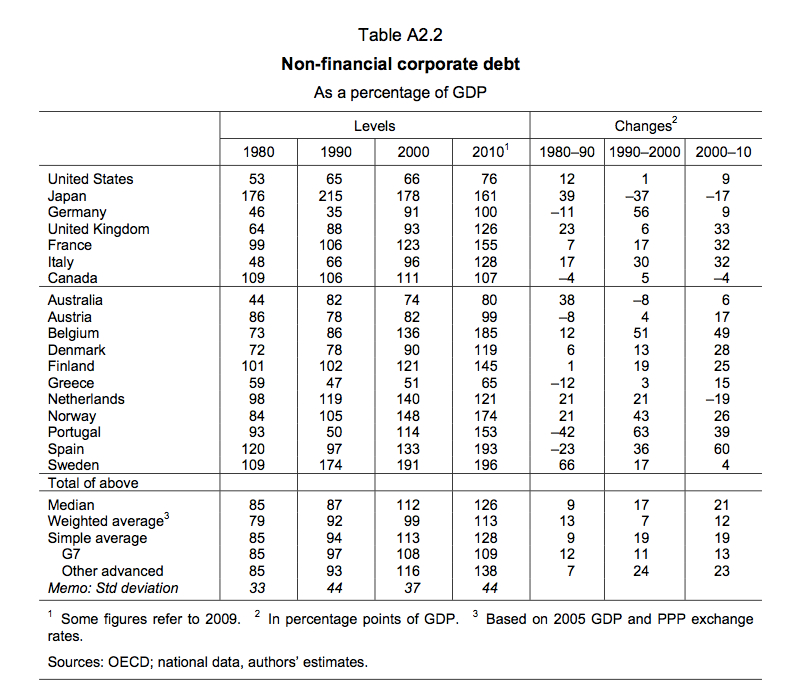

How about corporates? What will they do? And will they raise Japan’s long-term potential growth rate? Back to the Bank of Japan’s ‘Flow of Funds’, in which we see that Japanese corporations are not shy of borrowing from the bank.

And over to the BIS numbers, where we find 2010 debt a pretty substantial 161% of GDP, still one of the highest levels in the OECD.

The number has been falling, but his is because the corporate sector has been a net generator of cash for the last 20 years.

Has a lack of corporate credit been the source of a lack of corporate investment stunted growth? Jumping into the IMF’s International Financial Statistics database (here), we find that Japan has been investing a very steady 20% of GDP in gross fixed capital formation, of which over 60% has come from the corporate sector. This compares well with, say, Germany and the U.S., the current OECD stars of post credit crisis growth.

In other words, the idea that Japanese corporations have a plethora of shovel-ready, GDP-enhancing investments just sitting on the drawing board ready to go but for a lack of funding appears ridiculous. As the figures above show, corporates have been willing and able to invest significant sums from cash flow without resorting to bank borrowing. If they had wanted to expand their balance sheets through taking out more loans, they have had ample opportunity to do this already—but they haven’t and so they don’t.

So after round one of Kuroda’s easing, where will we get to? Well, I see a weaker yen as asset rich households and corporations move money offshore, and a bubbly stock market as equity is viewed as a one-way bet. For those without assets, all they will see is yen-depreciation related cost push inflation. So net, net this is a direct transfer of wealth from the asset poor to the asset rich.

More important, the entire modern capitalist system is founded on the assumption of growth. Without it, the system of governance and redistribution doesn’t work. It is for this reason that both monetary and fiscal policy have been taken to such extremes. But never have so few, done so much, to produce so little in the way of growth. And in so doing they have inadvertently rendered the entire system they are trying to protect even more brittle. I will return to all these themes in future posts.

I agree…good points. You didn’t mention what happens to the servicing of that debt the government holds when rates increase and the economy hasn’t grown fast enough to increase the tax receipts to pay the debt etc.. Thats the elephant in the room.. On the positive side however the weaker yen will helps exports a lot which will filter down to domestic suppliers and the suppliers of the suppliers and eventually the whisky bars and hostesses in Nagoya etc..That has been a powerful boost to the economy in the past and should not be under estimated. However i wonder how much less the impact might be now that global growth and demand is relatively weak and also japan’s competitors are much stronger now n terms of products etc…

Rambo: The only issue I have with the yen argument is that if Kuroda only wants to manipulate the currency then why didn’t the BOJ just buy U.S. Treasuries, rather than JGBs; i.e., a traditional FX intervention.

I guess through acting indirectly he can buy some time from the inevitable U.S. backlash, but I also sense he genuinely believes his preferred policy tools will unleash animal spirits at home unrelated to a cheaper yen. I think he will get the animal spirits nicely worked up, but those will be animal spirits of the asset bubble variety not of the GDP-enhancing type.

As for inflation, I don’t see this as a threat to government funding, since Kuroda has explicitly stated that he intends to take ownership of the JGB yield curve all the way out to 40 years. But this is severe financial repression, and will lead to imbalances elsewhere in the system. I want to write about this key topic in the future.