I have done a series of posts on U.K. flood risk which I think is of interest to any homeowner (or potential homeowner) with a property that could be affected by flooding. You can jump to the posts via the links or alternatively read the series as one long essay below.

- Flood Risk in the U.K.: What Does Mr. Market Think? (Part 1 Five Million Homes at Risk and Rising)

- Flood Risk in the U.K.: What Does Mr. Market Think? (Part 2 An Actuary’s Nightmare)

- Flood Risk in the U.K.: What Does Mr. Market Think? (Part 3 The Information Game)

- Flood Risk in the U.K.: What Does Mr. Market Think? (Part 4 You Ain’t Seen Nothing Yet)

Flood Risk in the U.K.: What Does Mr. Market Think? (Part 1 Five Million Homes at Risk and Rising)

Last week I attended an evening of talks given under the title “Extreme Weather and Floods” and hosted by the local sustainability group PAWS in the Thames side village of Pangbourne. The speakers were Professor Nigel Arnell, Director of the Walker Climate Institute, Reading University, and Stuart Clarke, Principal Engineer and the senior officer for flood risk management at West Berkshire Council.

At the close of the Q&A at the end of the evening, the moderator encouraged the audience to mingle with the speakers and take the opportunity to ask any follow-up questions. I ambled up to Professor Arnell to ask for a pdf copy of his Powerpoint slides. However, before I could get to Professor Arnell, he was grabbed by a late middle-aged man who wanted to vent his frustrations relating to his insurance company (I shall call him Mr. Angry). In short, the insurer was now demanding a £1,400 (about $2,100) annual insurance premium for flood risk cover and a £15,000 (about $23,000) excess for flood damage (the home owner has to pay the first £15,000 of damages before the insurer steps in). Result? He declined and his house now goes uninsured.

Flood insurance is a classic case of where climate change meets Mr. Market. At present, U.K. insurers have an agreement with the government known as the Statement of Principles on the Provision of Flood Insurance (a copy can be found at the Association of British Insurers here) that can be summarised as Mr Market Lite.

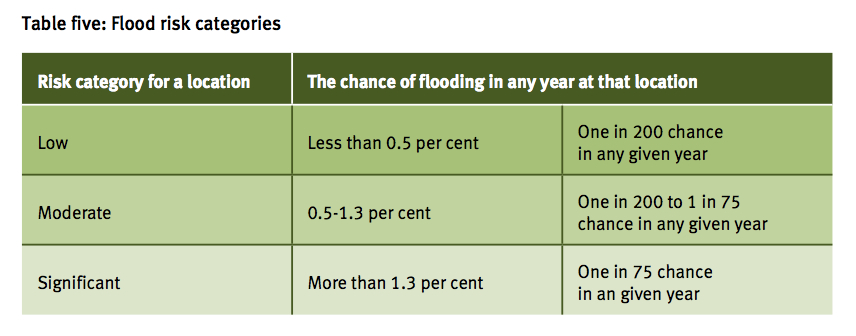

The border line between capitalism ‘red in tooth and claw’ and the socialization of risk is a one-in-75 year flood event (a 1.3% chance of flooding in an individual year). If you are in a flood zone which is estimated to have a flood risk greater than one in 75 years and the government has no plan to beef up flood defences over the next 5 years, then ‘tough’—you have to make an accommodation with Mr. Market. If—like Mr. Angry of Pangbourne above—Mr. Market’s quote is in the stratosphere, then you may be forced to turn it down and go uninsured. Note that if your property was built after 1 January 2009, it automatically falls outside of this agreement between the insurers and the government.

You can see the definitions of ‘low’, ‘moderate’ and ‘significant’ risk in the Environment Agency’s “Flooding in England: A National Assessment of Risk” here (click for larger image).

![]() Unfortunately, actions have consequences. The umbrella organisation of British house lenders, the Council of Mortgage Lenders (CML) made its position crystal clear in its submission to the government’s Pitt Review on Learning Lessons from the 2007 Floods (a pdf of the CML’s submission to the Pitt Review can be found here):

Unfortunately, actions have consequences. The umbrella organisation of British house lenders, the Council of Mortgage Lenders (CML) made its position crystal clear in its submission to the government’s Pitt Review on Learning Lessons from the 2007 Floods (a pdf of the CML’s submission to the Pitt Review can be found here):

There is a long standing link between the insurability and mortgageability of a property. Mortgage lenders offer a mortgage against the value of a property, normally with up to a 25 year contract to the borrower. It is a standard condition of all mortgages for the property to be covered by standard buildings insurance, including flood cover, for the full term of the contract, in order to protect the borrower and the lender. If insurance is not available, then it is unlikely that a property will be mortgageable.

And

A particular concern would be if the ABI were so dissatisfied with the government response to flooding that their members decided to withdraw cover from existing properties. Insurance contracts are normally only valid for 12 months, and if insurers did not renew cover at the end of this period, it would leave both lender and borrower exposed to an increased risk of loss and potentially invalidate the mortgage. The desire to retain flooding cover as a standard aspect of buildings insurance is, therefore, extremely important to the working of the mortgage market and the wider housing market. Properties that could not get either insurance or a mortgage would be significantly devalued.

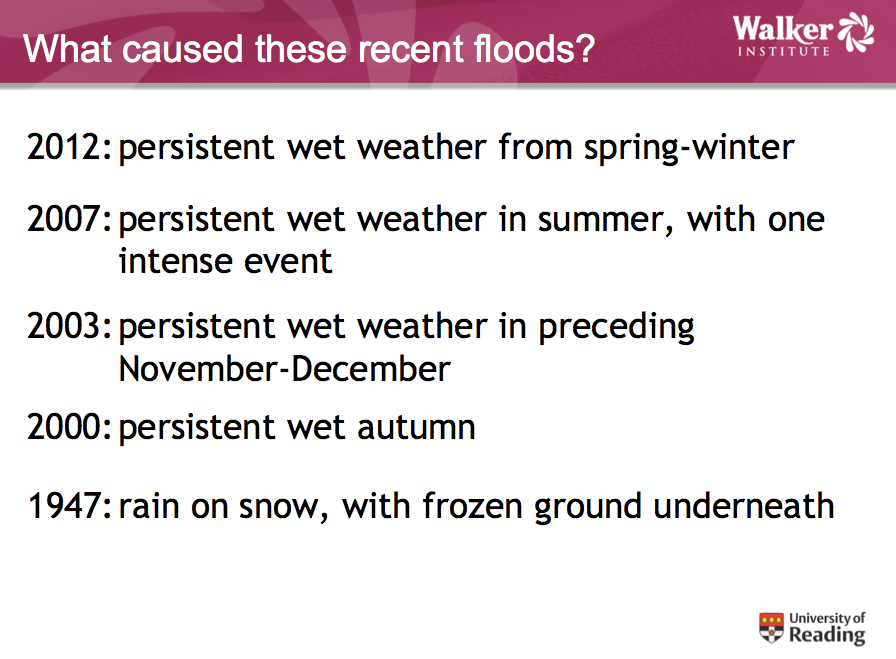

But why has the insurance industry chosen this time to back away from its agreement with the government. A slide from Professor Arnell’s presentation gives the answer:

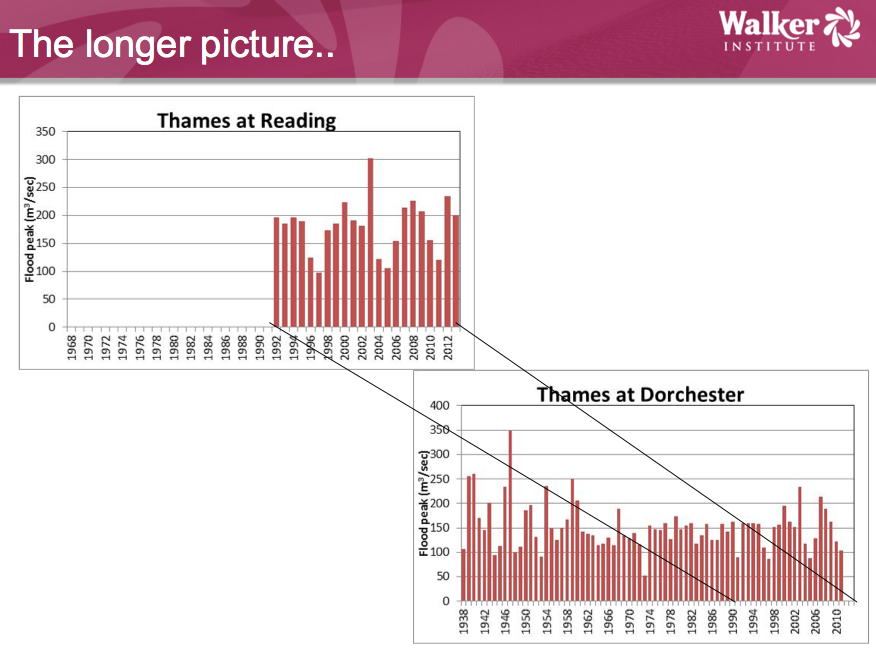

In short, a concentration of flooding events over the last 12 years. Nonetheless, Arnell also points out that clusters have happened before. The longest record of river flow is for Dorchester on Thames, which goes back to 1938. You can easily see the famous floods of 1947. A caveat is required, however. The Thames of the 1930s and 40s was very different from today; in other words, the flow was far less managed. Accordingly, we are not really comparing like with like when we look at the Dorchester on Thames time series below—the present river is not really the same river as the past.

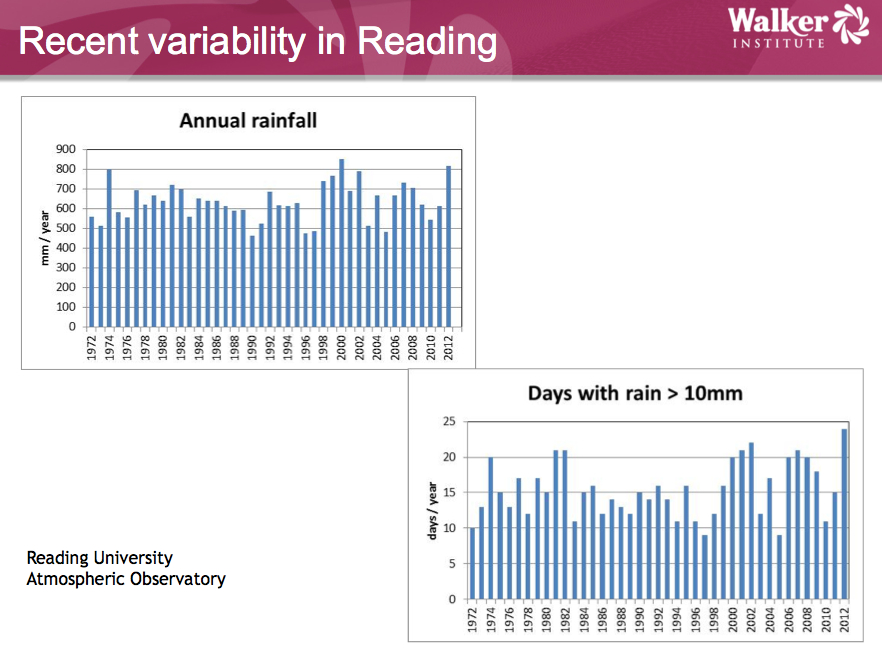

Rainfall may give a better feel for recent changes in climate, and the chart below shows rather tentative evidence of an uptick, mostly in the form of individual days with high rainfall.

So we have a cluster of flooding events and also some very tentative evidence of climate change showing up in the annual record. How does this translate into the insurance companies perception of risk? The starting point is their loss record, which is a critical driver of premiums. And the big event in this respect is 2007, when the industry paid out £3 billion according to the ABI. By contrast, ABI saw pay-outs of £1.2 billion in 2012.

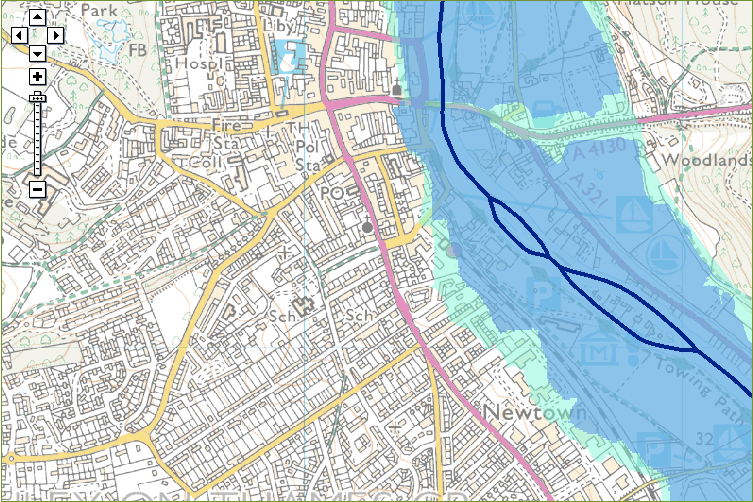

The year 2007 led to the Pitt Review of the U.K.’s flood preparedness and subsequent implication of most of its recommendations. In 2009, the Environment Agency published its latest National Flood Risk Assessment (NaFRA) that forms the underpinning for the one-in-75 year flood risk demarcation point and is provided to the insurers. Actually, NaFRA has 37 categories of risk all the way out to one in 1,000 events. Rather strangely, while the critical risk number is one in 75, the flood maps open to access by the general public show only one-in-100 risk and one-in-1000 risk areas. An example of the flood map of my home town of Henley is below (you can access the map for any area in the U.K. here). Dark blue is one in 100 and light blue/green is one in 1000 (note that for coastal areas, the dark blue area relates to a one in 200 food risk).

The flood maps have certain problems including the following:

1. They only relate to river, lake and sea-related flooding (fluvial flooding), not surface and groundwater related flooding (pluvial flooding). Also note the sea related risk numbers are different from the river ones on the maps.

2. The degree of detail only goes down to a scale of 1:10,000 and is searchable by postcode only, not by property.

3. The map doesn’t show depth of flooding, a key determinant of damage.

4. The map assumes that flood defences will work, and in 2007 many didn’t.

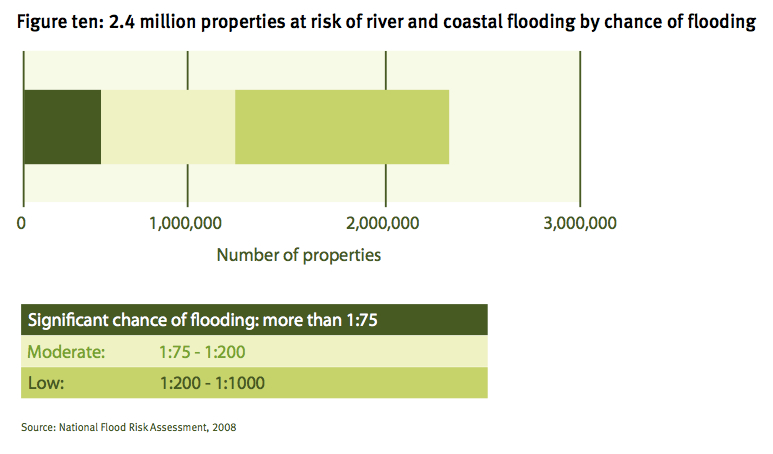

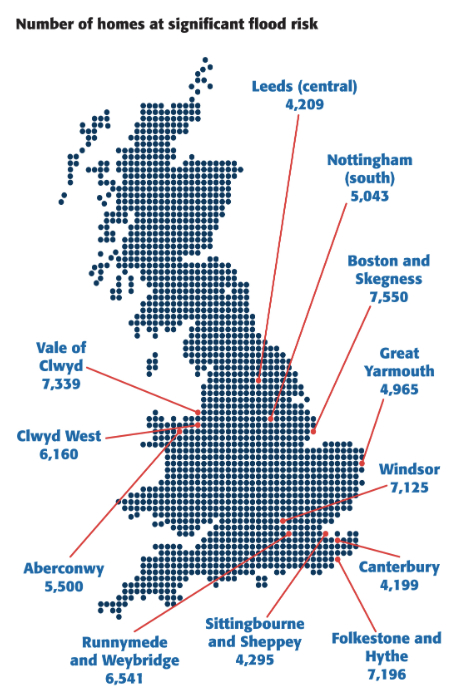

But let us start by assuming these NaFRA maps give a good assessment of risk. Then how many homes are we talking about (click for larger image)?

Low risk covers approximately 1.2 million homes, moderate around 900,000 and significant risk 330,000 (sea and river-related flooding). Moreover, another 3.8 million homes are at risk of surface water flooding according to the Environment Agency. As one million homes are exposed to both fluvial and pluvial, the grand total of homes at risk is 5.2 million, or one in six homes in England. Scotland and Wales add a few hundred thousand more homes.

As already stated above, the flood maps that can be accessed at the Environment Agency don’t cover surface water flooding—although the agency promises these will be made available in a couple of years. Moreover, this is a static assessment of risk and doesn’t take account of climate change. In the words of the Environment Agency (here):

The likelihood of flooding has been calculated using predicted water levels and taking the location, type and condition of any flood defences into account, whether or not they are currently shown on the Flood Map.

NaFRA is an assessment of flood risk based on information last updated in 2008. It shows the likelihood and consequences of flooding that could happen now. It does consider climate changes that have already happened but it does not show how the risks will increase in the future due to climate change. However, we are planning to develop and use this method to determine how flood likelihood may change in the future with climate change.

It is worth bearing in mind that the potential extent of an extreme flood shown on the Flood Map might in future become more ‘normal’ as a result of climate change.

Fortunately, the UK government’s Department for the Environment, Food & Rural Affairs (DEFRA) published a report entitled Climate Change Risk Assessment (CCRA) in 2012. In the section entitled “Climate Change Risk Assessment for the Floods and Coastal Erosion Sector” we see these numbers:

The number of properties at risk of flooding (with an annual probability of 1.3% or greater) from rivers or the sea in England and Wales is projected to increase from the baseline of about 560,000 (370,000 residential and 190,000 non-residential) to

– Between 800,000 and 2.1 million by the 2050s of which between 530,000 and 1.5 million are residential properties

– Between 1.0 million and 2.9 million by the 2080s of which between 700,000 and 2.1 million are residential properties.

These are huge numbers of homes at risk (and they are really a stab in the dark, to which theme I will return to in another post).

Moreover, we have only been looking at one side of the risk equation through most of this post: probability. True risk is probability times effect. If there is a one in ten chance of your home flooding and each flooding event produces £50,000 of damage, then it is not surprising the insurance industry wants to hike your premiums, increase your excess—or, better still, not insure you at all.

Against this background, we now have a merry dance between property owners, insurers and the government over who holds the risk. How realistic are the CCRA numbers above? Are they good enough numbers to base hard-nosed insurance decisions around? I will return to the theme of how much true risk is out there and who gets to hold it in part 2, 3 and 4 of this post.

Flood Risk in the U.K.: What Does Mr. Market Think? (Part 2 An Actuary’s Nightmare)

In my previous post, I noted that strange things were happening in the flood insurance market. In short, the insurance industry no longer wants to extend the status quo (here):

The current agreement under which insurers continue to offer flood insurance to their existing customers will expire on 30 June 2013. The insurance industry has proposed a new a scheme to ensure customers can still buy affordable flood insurance, after this date. We are currently in talks with the Government about taking this forward.

In truth, they want to move some flood risk from one actor in the market to another. But before I look at that issue, I want to ask the question “why do they want to change the status quo?”

To do this, we need to take a quick detour through the theory of insurance. There is a nice little eight-minute youtube video that explains the theory of insurance here:

The core message in the video is the same as the core message of this blog: risk is the probability of an event times the cost of the event.![]() When we buy insurance, we generally are buying insurance for a low probability, high cost event. A horrible spiky risk; so if you are unlucky on the roulette table of life, a single event can rampage through your finances. But an insurer, by pooling hundreds of thousands of such single spiky risks, can make them smooth and well behaved.

When we buy insurance, we generally are buying insurance for a low probability, high cost event. A horrible spiky risk; so if you are unlucky on the roulette table of life, a single event can rampage through your finances. But an insurer, by pooling hundreds of thousands of such single spiky risks, can make them smooth and well behaved.

As the video above notes, the insurer’s friend is the actuary, whose job is to calculate how those single spiky events look like when pooled together. If you like maths, then I highly recommend this short paper on Risk and Insurance published by the Education and Examination Committee of the U.S. Society of Actuaries (SOA). It takes the video above up a few levels.

Just to repeat, risk has two components. SOA calls these frequency and severity.

This random variable for the number of losses is commonly referred to as the frequency of loss and its probability distribution is called the frequency distribution……..The second random variable is the amount of the loss, given that a loss has occurred. The amount of loss is often referred to as the severity and the probability distribution for the amount of loss is called the severity distribution. By combining the frequency distribution with the severity distribution we can determine the overall loss distribution.

So the insurer is going to call in an actuary and ask two key questions: if I insure a bunch of homes for flood, how often are they going to get hit by floods, and when they are hit, how much will it cost? So how does an actuary answer these two questions? The first thing they will do is look at their database of past events. This will give them a first cut at the ‘frequency distribution’ (how often flood comes) and the ‘severity distribution’ (how much flood costs).

As a blogger, I absolutely loath those bloggers who use full caps to put a point across. It seems shrill and crass to me. But today is an exception. The holy grail of every actuary are frequency and severity distributions THAT ARE STABLE. If the distributions are stable, you can use the past to tell you things about the future.

So back to the Environment Agency and the National Flood Risk Assessment (NaFRA). Note that NaFRA is a frequency distribution; it doesn’t say anything about the severity distribution. Is the frequency distribution as published by NaFRA stable? Unfortunately, no. Between each update of the NaFRA, homes move between the various risk categories, with the progression being from lower risk to higher risk. Moreover, as I noted in my previous post, the Environment Agency is not incorporating climate change into its risk assessment. So if you could ask them what your flood risk is currently, they will tell you what is was yesterday, not what it will be tomorrow.

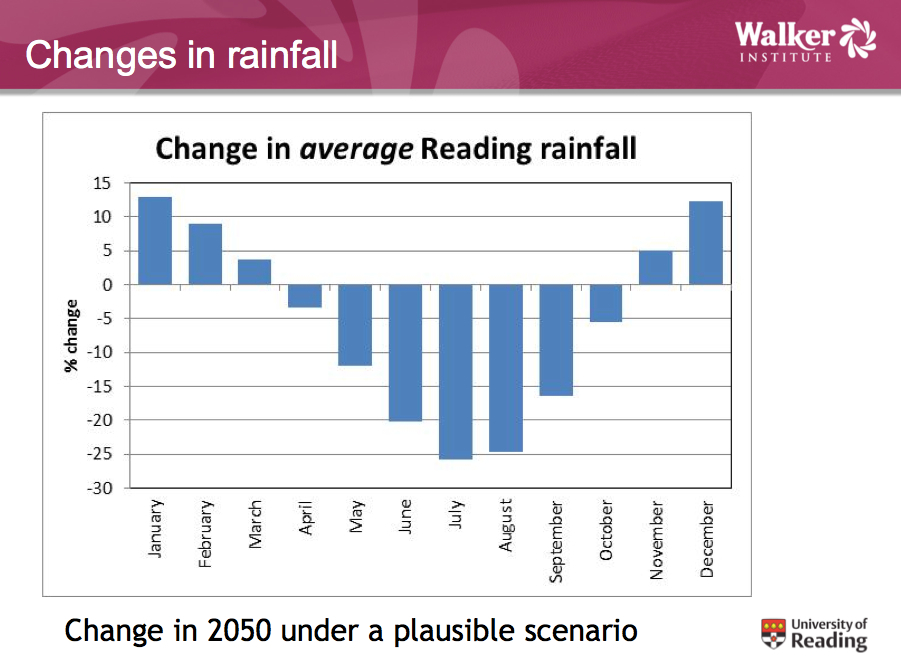

Let’s now revisit some slides from Professor Arnell’s presentation that I talked about in my first post. These tell us that climate chance is, implicitly, going to move the frequency and severity distribution in future years.

As one of Arnell’s previous slides highlighted (in my previous post), you can get floods either through intense events or chronic events. So remember these are percent changes. Just because we have dry summers doesn’t mean we can’t get inundated in winter. So this says that the hoped-for-stable frequency distribution of the actuary will wonder around. But it gets a lot worse.

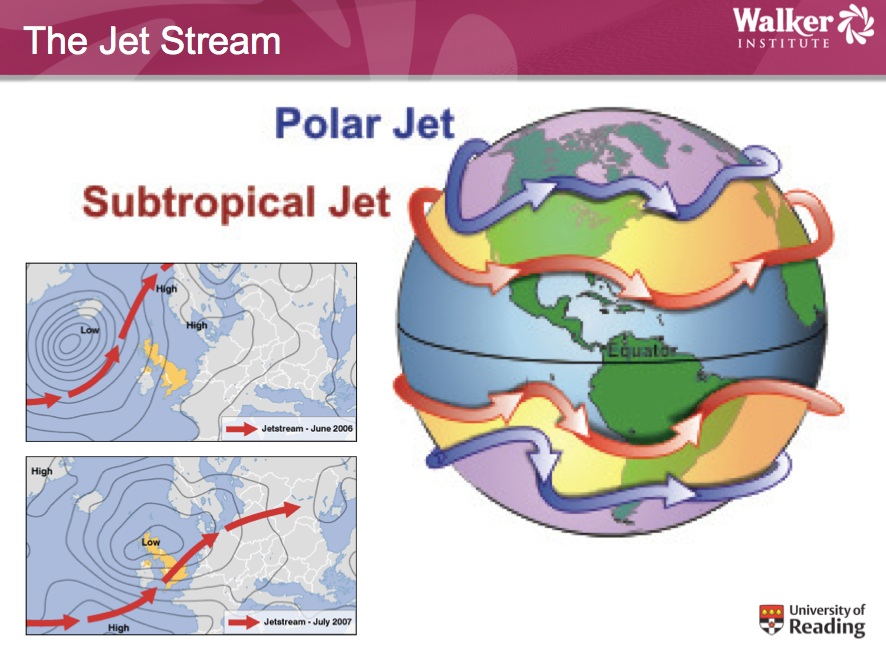

For a start, this is a ‘plausible scenario’. An actuary could just about stomach a frequency distribution moving from one stable state to another, but this is not what is happening. Professor Arnell has some other slides, which are what I would call ‘snap shots of climate change theory work in progress’. They show a jet stream that has become increasingly unstable:

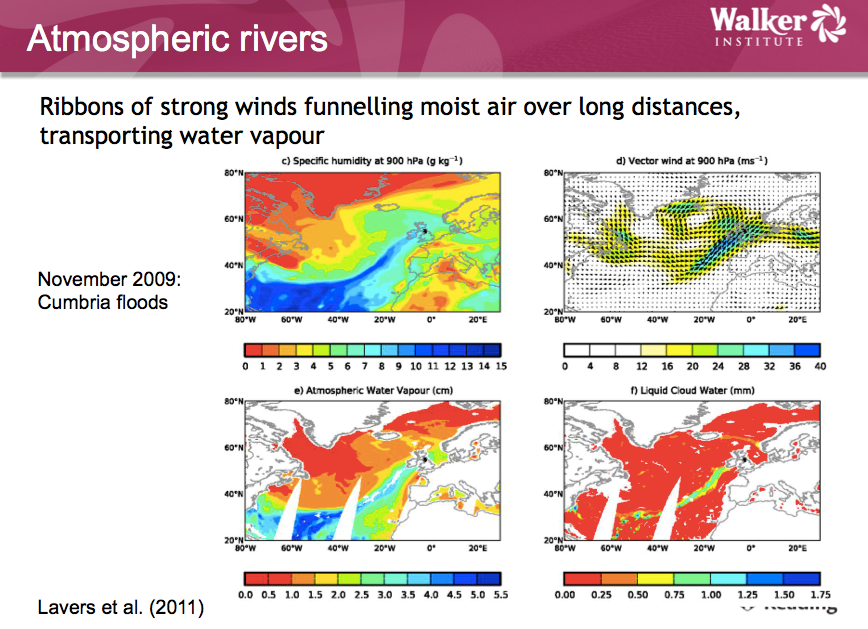

And atmospheric rivers challenging moist air from one region to another:

This is climate change theory being put together in real time. For example, it was only in 2007 that Arctic sea ice extent drastically diverged from its expected path, in the process putting large swathes of sea into an ice free state at certain times of the year. And it is only recently, that attention has focussed on instability of the jet stream, with a flurry of academic papers linking this to the warming of the Arctic.

That is at the macro level. At the micro level, Professor Arnell’s presentation brought home to me the sheer variability of flood risk at particular localities. The village of Pangbourne has a variety of catchments that all have different characteristics. Accordingly, slightly different permutations of rainfall intensity and perseverance in slightly different localities can give rise to very different flooding outcomes. The actuary really doesn’t like this. They want independent and identical random variables for the efficient modelling of risk. If they don’t get them, their overall loss distribution stretches out with big, fat risk tails. The type of tail that produced the £3 billion plus loss in 2007. And what to do in this situation? Easy: Cut that tail off. Don’t insure Mr. Angry of Pangbourne who we met at the beginning on my first post on the topic.

So what to do in this insurance game? Well, first recognise the asymmetry of information. The insurance companies are currently recognising that they don’t know the future shape of risk (and they don’t like it)—that is why they are so keen on passing the risk over to the government. By contrast, most home owners haven’t the faintest clue that they don’t know the unknowns.

In my next post, I want to drill down a little into that asymmetry of information between insurers and home owners, and how the insurance industry wants to change the rules.

Flood Risk in the U.K.: What Does Mr. Market Think? (Part 3 The Information Game)

In my last post, we saw that the insurance industry has broken with the status quo because it realises that flood risk has entered into a new era. The stable frequency and loss distributions that underpinned their actuary-led calculations of the past are no more. The loss-related data that the industry laboriously collected in the past only gives insurers a limited ability to look into the future.

Nonetheless, if we only think of the pure insurance risk (as opposed to an insurer’s business model risk), insurance companies are really looking out only one year: when a home owner’s policy comes up for renewal each year, the insurer has the opportunity to change the terms and conditions of the policy including the premium and excess. And they could change the terms and conditions very aggressively—the equivalent of suspending coverage, just in disguise.

Given these factors, if an insurer can look out for that one year and capture a decent understanding of the risk, it should be protected from any massive loss event that blows it out of business. And if there is a big loss event and the insurance company is still standing, it can subsequently change the terms and conditions of the outstanding policies at the next yearly renewal including a hefty hike in the premiums.

Up until the floods of 2007, with their £3 billion-plus associated insurance pay-outs, the information in the hands of an insurer and a well-informed home owner would have not been that much different. Both would have had access (and still do have access) to the Environment Agency (EA)’s flood maps.

The flood maps are updated quarterly and give a risk assessment at the one in 100 and one in 1000 flood probability levels for river flooding (an EA pamphlet on the flood map can be found here). On top of this, the EA provides the insurance industry with the National Flood Risk Assessment (NaFRA) data. As mentioned in a previous post, this is more specific in terms of its flood risk categories (an EA pamphlet on NaFRA can be found here) and underpins the Statement of Principles agreement between the Association of British Insurers and the government. I will repeat the risk category definitions once again:

- Low risk: the chance of flooding each year is 0.5 per cent (1 in 200) or less

- Moderate risk: the chance of flooding in any year is 1.3 per cent (1 in 75) or less but greater than 0.5 per cent (1 in 200)

- Significant risk: the chance of flooding in any year is greater than 1.3 per cent (1 in 75)

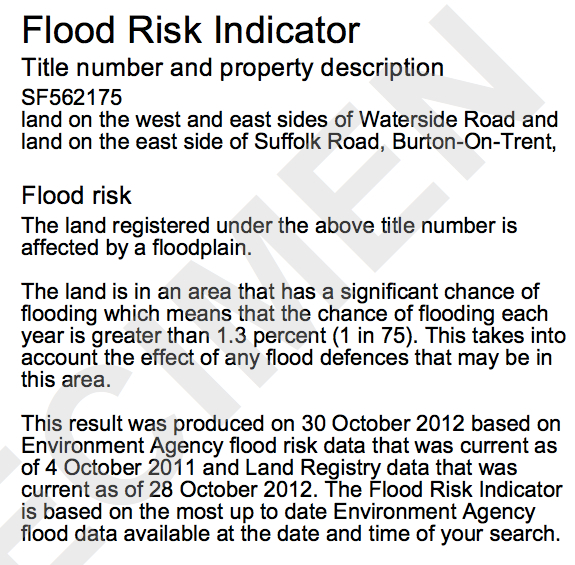

A home owner may have more interest in the one-in-75 risk (available from NaFRA) rather than the one-in-100 risk (available from the EA on-line Flood Map) since this is the demarcation point used to differentiate between ‘significant’ risk and ‘moderate’ risk, and as a result drives insurance premiums levels. Moreover, this risk demarcation point gives an some indication of what ‘significant’ risk property owners may be in for after the expiry of the Statement of Principles agreement expires in June 2013.![]()

Fortunately, a risk assessment (called the Flood Risk Indicator, a description of which can be found here) based on NaFRA became available to the general public in 2009 through the Land Registry here and and costs £9 (although you can actually get the same information for free by contacting the EA directly). An example is below:

Now we need to recall the limitations of NaFRA, and accordingly the Land Registry’s Flood Risk Indicator:

- The degree of granularity of the data is limited. NaFRA goes down to a land area cell size of 100 metres by 100 metres, not down to an individual property

- NaFRA is a frequency distribution: it says nothing of loss, and loss is principally driven by depth of flood, which is not covered by NaFRA

- NaFRA does not cover surface water flooding

- NaFRA does not cover groundwater flooding

- NaFRA only looks at climate change that has taken place at the time of the survey date not beyond. So given the last NaFRA assessment was made in 2008, it is gradually going out of date

Because of the 2007 floods (when surface water flooding caused 50% of the flooding and 75% of the damage by value), the insurance industry has turned to the private-sector to fill the numerous holes in the Environment Agency’s risk assessment (NaFRA).

Against this background, a significant asymmetry of information has emerged between insurers and home owners. Until recently, either party could access the same flood risk data (although the insurance industry would have had its own loss data). Now, insurers are buying a whole range of data and analysis that home owners don’t get to see (at least without paying significant sums of money).

Specifically, insurers are purchasing data sets from such firms as JBA, RMS and Ambiental that a) give surface water risk, b) provide more detail than NaFRA’s 100 metre by 100 metre squares and c), in some case, offer predictions on potential depth of flooding. Moreover, ground water flood risk data is being made available by the British Geographical Survey (BGS) on a commercial basis here. Finally, firms such as Argyll Environmental have sprung up to provide consulting services that blend all the available information together.

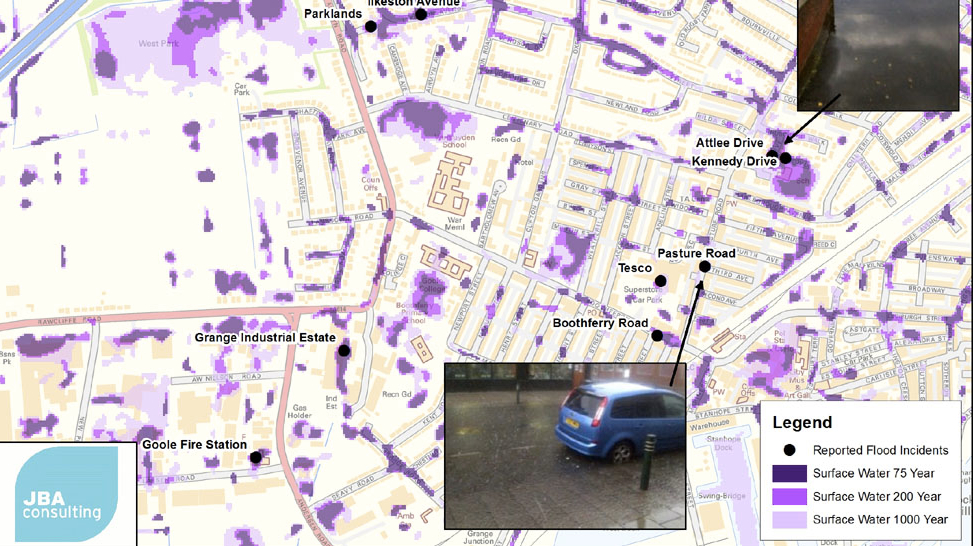

To give you a sense of what insurers can potentially see, the image below is taken from a JBA submission to the MacRobert engineering awards. The level of detail is far and beyond anything in the Environment Agency’s flood maps.

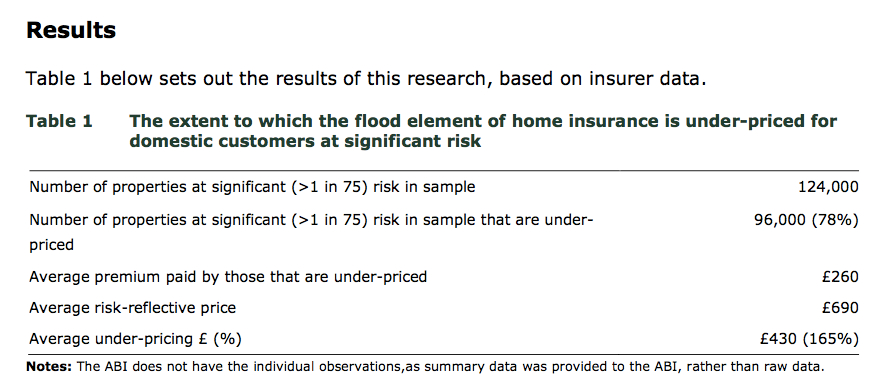

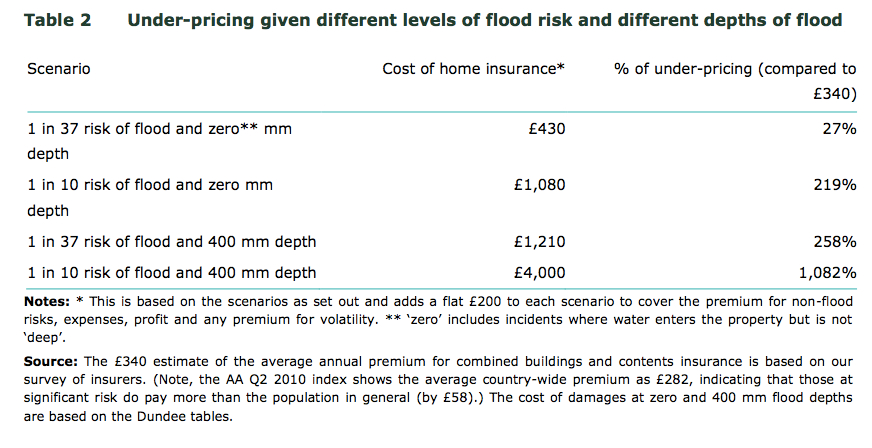

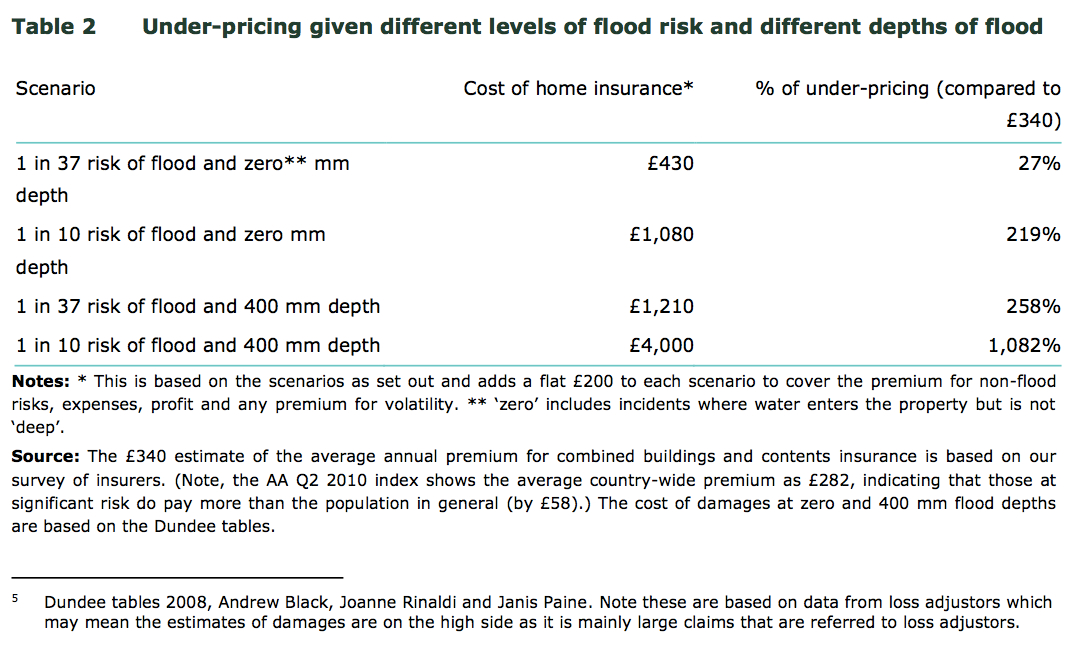

Critically, with better data the insurers are in a position to calculate where policies within the Statement of Principles agreement with the government are being mispriced. A research brief by the ABI dated January 2011, gives us some numbers on the general underpricing of ‘significant’ risk properties (click for larger image):

And also how underpricing changes when frequency of flood worsens and the severity risk (as proxied by the height of the flood) increases:

The analysis above has an interesting hole: if ‘significant’ risk properties are being underpriced insurance premium-wise, then other properties are being overpriced. The £430 in the first table has to go somewhere, either as a burden on other property holders or as a drag on insurance company profits. Note also that the 124,000 properties are a sample, not the actual population of insured significant risk properties.

In reality, the industry has explicitly stated before that such underpriced risks are being parcelled out to property owners in low risk areas. This is one form of the socialisation of risk. Such actions, however, give rise to the problem of adverse selection. According to Wikipedia, the ABI covers 94% of insurance-related service provision in the U.K., but it is still worried that new entrants can cherry pick low or no risk householders by offering them policies that include none of the implicit subsidy in the policies offered by ABI members under the Statement of Principles.

But as we previously mentioned, the Statement of Principles says nothing about the size of premiums, level of excess and conditions of insurance policies. In short, it is a vague promise to be nice to property owners in significant-risk areas. In the ABI’s words:

It is important to note that the premiums charged and policy terms will reflect the level of risk presented and are not affected by this commitment.

So if you happen to live in a property at significant risk such as those in the Insurance Age article below, you basically are at the mercy of your insurance company’s forbearance.

And if the ABI wished, it could gut the Statement of Principles without actually cancelling it by hiking premiums and putting up excesses. However, it doesn’t want to go down that road. Why? Well, to be fair, the ABI may worry about the fate of the 200,000 or so ‘significant’ risk households (and counting upwards as climate change winds its merry way) that may lose access to flood risk insurance (and thus the ability to secure a mortgage loan) in the years to come.

And then again the industry may worry about the political risk. Mr Angry of Pangbourne, who we met in my first post, is in a deep funk. And I am sure he is already venting at one or more of his local council, district council, the Environment Agency and/or local MP.

As climate change progresses and the risk tools of the insurance companies improve, expect more Mr. Angry types to be created. Further, what will the collective noun of Mr Angry types do? Very likely pack together to become The Very Angry Owners of At-Flood-Risk Houses Association. Actually, they already have some outlets to collectively vent in the form of Know Your Flood Risk and the National Flood Forum (although the former has rather opaque roots and the latter was partially founded by the government and thus has the wisp of a Russian union organisation in the old Soviet era). However, I expect that as their numbers growth, and anger rises with each successive flood, they will become a much more irate political pressure group.

Against this background, let us turn to what the ABI is proposing post the expiry of the current arrangement in June 2013. The ABI’s submission to the UK parliament provides a nice summation here. At the core of the industry’s proposal is a not-for-profit flood reinsurance fund:

The fund would be a major improvement on the SoP (Statement of Principles) as it would deliver a competitive market where consumers have real choice whilst ensuring homes at risk of flooding are able to buy affordable flood cover. The fund would provide flood insurance for the 1- 2% (~200,000) properties in the UK where accessing flood insurance in an open market would be problematic. The remaining 98% of properties would continue to be covered by the industry as normal.

And to the important question of where the money for the fund would come from?

To make sure that the fund had sufficient money in it, insurance companies would make an annual contribution based on their level of premium income in the form of a levy raised from all insurance premiums. This would complement the income to the fund from the flood premiums from the high flood risk properties in the scheme.

This is not very different from the current arrangement under which ‘significant’ risk properties get an implicit subsidy from ‘low’ risk ones. But with a twist:

While the losses could be smoothed through reinsurance, in the event that not enough funds had built up in the first few years to cover a major incident like the 2007 floods, there would be a deficit needing to be met (effectively a need for an overdraft facility). Exceptionally large losses, such as a catastrophic North Sea tidal surge, may exceed this. We are currently discussing the model with the Government, and one of the key aspects of the negotiation is how we can work together to manage the liabilities of the scheme and raise the funds needed by the pool to operate, and well as the assurances insurers need about investment in flood defences to commit to the solution.

Now at first glance, this doesn’t look revolutionary. If the government is only extending an ‘overdraft facility’, then the industry could hike premiums following a 2007-type event and pay back the government. A problem arises, however, if a) 2007-type events start appearing with increasing frequency (which they likely will with climate change) or b) super 2007-type events occur (which they also probably will with climate change). Let’s say these super 2007-type events are equivalent in damage to a catastrophic North Sea tidal surge (which happens to be mentioned by the ABI above). The wording in the submission to parliament is suitably vague, but suggests that such events will produce losses above the government’s overdraft facility and……? They can’t quite bring themselves to say it, but I think the answer is pretty clear: the government picks up the tab.

So to recap, my previous post suggested that the insurance industry is grappling with frequency and severity distributions that have become unstable and have flattened out. So the industry’s overall loss distributions is growing a big, fat tail. The industry can only deal with this expanding tail by chopping it off. They can not extend insurance to the growing band of ‘significant’ risk customers—or bring in outrageously high premiums and excesses which is basically the same thing. Alternatively, they can give the tail to someone else, preferably the government.

Moreover, as the information asymmetry between householders and insurers has grown over the last 5 years, the industry now knows who is in the tail of negative outcomes (and who is likely to migrate into this tail over the coming years as climate change progresses)—while the vast majority of home-owners don’t.

In my final post, I will take a look at what happens to valuations on flooded houses and take a closer look at how climate change is making the risk pass the parcel game between home owners, the insurers, local councils and the central government ever more intense.

Flood Risk in the U.K.: What Does Mr. Market Think? (Part 4 You Ain’t Seen Nothing Yet)

The National Flood Risk Assessment (NaFRA) of 2008, conducted by the Environment Agency (EA), calculates that 330,000 properties are at ‘significant’ risk (defined as one in 75 years) of fluvial flood in England. The survey is a bit long in the tooth nowadays, and I expect that if they repeated the assessment exercise today, more houses would fall into the ‘significant’ risk category.

In a similar vein, The Association of British Insurers’ (ABI) submission to the U.K. parliament talks of around 200,000 homes (some 1 to 2 percent of the total housing stock) that would now find it difficult to obtain flood insurance if open market conditions solely determined availability (and if they can’t get insurance, they won’t be able to support a mortgage).

For climate change “skeptics” who believe in free markets, the fact that the British insurance industry takes climate change as a given, and has done so for many years, is a difficult fact to face. In a forward to a report called “The Changing Climate for Insurers” back in 2004, The ABI’s then Head of General Insurance John Parker was unequivocal:

Climate change is no longer a marginal issue. We live with its effects every day. And we should prepare ourselves for its full impacts in the years ahead. It is time to bring planning for climate change into the mainstream of business life.

What the ABI is doing through requesting the government to create a new insurance arrangement after the expiry of the Statement of Principles agreement in June 2013 is to “prepare ourselves for (climate change’s) full impacts in the years ahead”. We can hardly say we were not warned.

We can also hardly say that climate change is alarmist nonsense or a socialist plot. The insurance industry is about as close to “red in tooth and claw” capitalism as one could get. And the message from Mr. Market in his insurance industry incarnation is very clear: climate change is coming to a place near you very soon—get used to it.

Yet the ABI has blurred the line between uninsurability and unafordability. Tim Hartford in his Financial Times’ “Undercover Economist” column sets out three hard-to-insure risks. First, genuine unknown unknowns, where the insurer has no idea of the shape of the frequency distribution and severity distribution. Second, the adverse selection situation, where there is an asymmetry of information acting against the insurer: those who know they are bad risks use their effective insider knowledge to seek out and profit from insurance. Finally, insurance that is just expensive. He puts flood insurance into the final category:

Now the third kind of hard-to-insure risk is stuff that’s expensive and happens quite often. I’m trying to buy a house, I’m nearly 40 and so I’m trying to buy insurance for my family in case I die or become too ill to work. This is perfectly possible: it’s just expensive, because it’s not unusual for middle-aged men to get seriously ill. This sounds like a much better description of allegedly uninsurable homes: if there is a one in five chance of a flood, and a flood is going to cost £50,000, don’t expect to pay less than £10,000 a year for flood insurance.

…..but unaffordability is not uninsurability. It’s insurable but expensive.

If these homes actually were uninsurable the government would need to step in and cut some kind of deal with the insurance industry – exactly the kind of deal that has lasted for the past few years and seems about to unravel. But if the problem is unaffordability, trying to solve it by cutting a deal with the insurance industry is just a way of obscuring what is really going on. The real solution is simple and stark: the government needs to decide whether it wants to pay people thousands of pounds a year to live in high-risk areas or not.

And in austerity Britain, no Chancellor of the Exchequer really wants to shoulder these extra payments.![]() Hartford goes on:

Hartford goes on:

If (the government does not want to pay), then people who currently live in flood-risk areas will see the price of their homes collapse…..

……To whatever price would tempt people to live somewhere that was not only prone to distressing and disruptive floods, but was also hugely expensive to insure. Which in extreme cases will be “zero”.

The charity the Joseph Rowntree Foundation in its March 2012 Viewpoint Report entitled “Social Justice and the Future of Flood Insurance” describes Hartford’s preferred approach as ‘individualist, risk-sensitive insurance’ as opposed to their preferred approach called ‘solidaristic, risk-insensitive insurance’.

Personally, I prefer to call a spade a spade: what we are talking about here is the socialization of risk, or alternatively we could call it the socialization of insurance-related losses. The word ‘solidaristic’ just appears a euphemism to me. But that is not to be judgemental. The right as well as the left appear desperate to keep the word ‘socialization’ hidden in the closet. For example, when the well-heeled Thames Valley occupants of river-front properties write to their local Conservative Party MPs to complain about their treatment at the hands of their insurers, I am sure the letters will contain few passages calling for the socialization of risk. So ‘individualistic, risk-sensitive insurance’ has few natural supporters among home-owners.

The Rowntree Foundation, however, goes on to define three types of fairness: 1) actuarial (espoused by Tim Hartford and Mr. Market), 2) choice-based and 3) social justice.

The choice-based distinction appears a bit of a diversion to me: few people consciously choose to buy a house with the potential for repeated episodes of flooding. Perhaps, as with all things climate change, many people chose not to know by failing to deepen their knowledge of climate change, but this seems an impractical basis on which decide whether any individual property on a flood-prone street gets insurance cover or not. Further, we must always remember the terrifying speed with which climate change has appeared on the horizon as a major social- and economic-policy issue. The Intergovernmental Panel on Climate Change (IPCC) was only created in 1988, and the issue has still not fully made the transition from academia to the general public. So I think few people have knowingly decided to take their chances with climate change when it comes to flood.

So given the foundation’s mandate to support society’s disadvantaged, it is not surprising that social-justice fairness is proposed as the governing philosophy, and ‘solidaristic, risk insensitive’ insurance as the preferred option. Whether the Labour Party will adopt the same approach we do not know. To date the only utterances I have heard from them on the subject are criticisms of the ruling coalition government for prevarication in reaching an agreement with the ABI. Ironically, a Labour Party victory may be Mr. Angry of Pangbourne on Thames’ best bet to get insurance cover reinstated at a reasonable cost. But even if the Labour Party does adopt the flood-risk socialization principle (or its euphemism-laden equivalent), I still see trouble ahead.

The trouble comes from the degree to which climate change will distort the insurance companies’ frequency and severity probability distributions as we go out beyond a year or two. Unfortunately, data in this area appears sorely lacking. The best data we have comes from Climate Change Risk Assessment (CCRA) published by the Department for Environment and Rural Affairs in January 2012. (Note that the CCRAs will come out in a five-year cycle, so we have no update until 2017.)

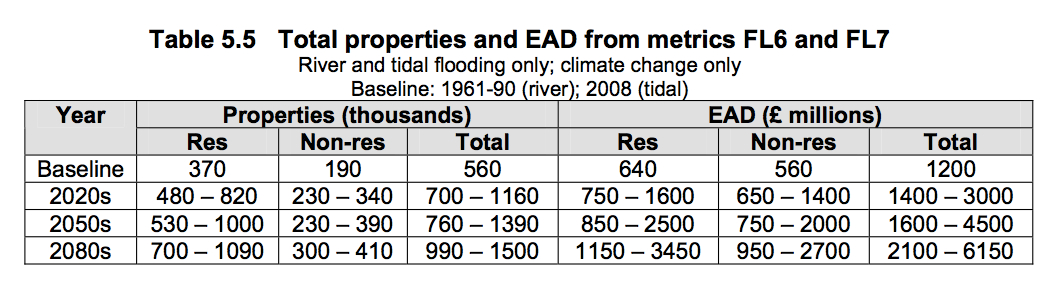

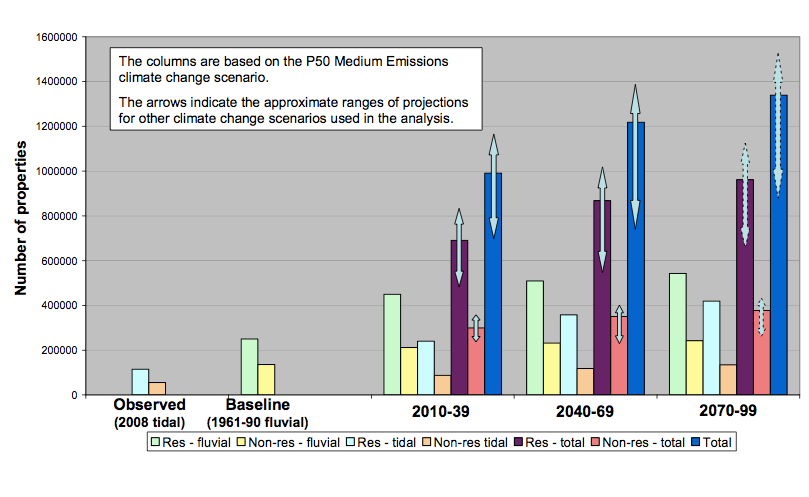

The CCRA shows the total number of residential properties subject to ‘significant’ risk of flooding rising from 370,000 today (actually at the time of the last NaFRA in 2008) for England and Wales to 700,000 to 1,160,000 by the 2020s (click for larger image).

You can see these numbers graphically here:

Accordingly, the estimated annual damage (EAD) will likely rise from £640 million now to £750 million to £1.6 billion (all at current prices) in the 2020s. However, these numbers have a plethora of holes. First they refer to fluvial flooding only. The CCRA is quite clear about this:

These figures cover tidal and river flooding, but not surface water flooding….

….There are estimated to be more properties exposed to the risk of surface water flooding than river and tidal flooding. There is therefore an urgent need to develop projections of future surface water flood risk for the next CCRA.

This paper argues that major gaps exist in the research and policy understanding of the intersection of flood risk, climate change and housing markets. When extrapolating the research on historical flooding to the effects of future floods – the frequency and severity of which are likely to be affected by global warming – housing economists must be careful to avoid a number of methodological fallacies: (a) The Fallacy of Replication, (b) The Fallacy of Composition, (c) The Fallacy of Linear Scaling, and (d) The Fallacy of Isolated Impacts. We argue that, once these are taken into account, the potential magnitude and complexity of future flood impacts on house prices could be considerably greater than existing research might suggest. A step change is needed in theory and methods if housing economists are to make plausible connections with long-term climate projections.

This all sounds very technical, but in actual fact it isn’t. And I urge anyone of thinks they may possibly be in a-one-75- year ‘significant’ risk, or worse, property to read this report. The ‘Four Fallacies’ deserve a quick exposition at least:

a) The Fallacy of Replication: “Properties that currently experience floods are of type x and not type y. Therefore, properties that experience floods in the future will also be of type x, and not type y.”

As an example, your well-heeled owner of £2 million Thames side property already knows about flood risk and has defended against it. Further, the property will always retain an amenity value that only a river-front property, with its charming boat house, can provide. The properties 5o metres back are, in effect, subject to ‘virgin risk’; they are sub-prime properties relative to the riverfront prime, and are not set up to absorb the impact of a full-blown flooding event that goes beyond the river front (which will inevitably happen).

b) The Fallacy of Composition: “Significant financial safety nets are viable if a single area is flooded. Therefore, significant financial safety nets will be viable if all areas are flooded.”

This has been a recurrent theme of this entire blog series. We have had a system priced off a long-lasting status quo. And now the ABI says the status quo cannot continue. In the words of The Adam Smith Research Foundation:

Existing major UK floods occurred in a financial environment that ensures prospective buyers of flood-liable properties will be able to obtain both insurance and mortgage finance. It is perhaps not surprising that price effects have so far been negligible and temporary. However, once this regime starts to break down, the price effects of floods could be marked, most notably in those flood- prone neighbourhoods abandoned by insurers and mortgage lenders.

c) The Fallacy of Linear Scaling: “The impact of a flood of severity y, is of magnitude z. Therefore, the impact of a flood twice the severity of y, will be twice the magnitude of z.”

The authors pick out three examples under this heading, but I will just highlight one, since I have a keen interest in the psychology of risk:

Humans have a tendency to underestimate risks that appear distant or global, or which others seem to accept without concern (Kousky & Zeckhauser, 2006). Recent studies indicate that buyers may not have full information about properties due to high search costs and sellers’ unwillingness to reveal information about dis-amenities such as flood risk (Chivers & Flores, 2002; Lammond, 2009).

Disclosure of flood risk is therefore likely to decrease market value (Troy & Romm, 2004; Pope, 2008). While individuals may underestimate flood risk, this may not be true if floods become frequent and ubiquitous, because flood events raise people’s awareness of potential risk (Bin & Polasky, 2004).

Even in years when a particular dwelling is not flooded, the prevalence of flooding elsewhere, communicated via accounts in news reports and social dialogue, will act as constant reminders of the household’s flood risk. People will not forget because the climate and media will not permit them; and the bounce-back effect will become a thing of the past (Pryce et al., 2011).

d) The Fallacy of Isolated Impacts: “The price of house A is reduced because it is flooded. House B is not flooded and, therefore, its price will not be reduced, irrespective of its proximity to A.”

This is really just common sense. You only need one part of the neighbourhood to be impaired in order to impact on the value of the entire neighbourhood.

The report ends with something that seems obvious to me, but I am amazed by how few have absorbed it:

Unfortunately, the housing economics literature on floods has so far developed largely under the assumption of climatic stability.

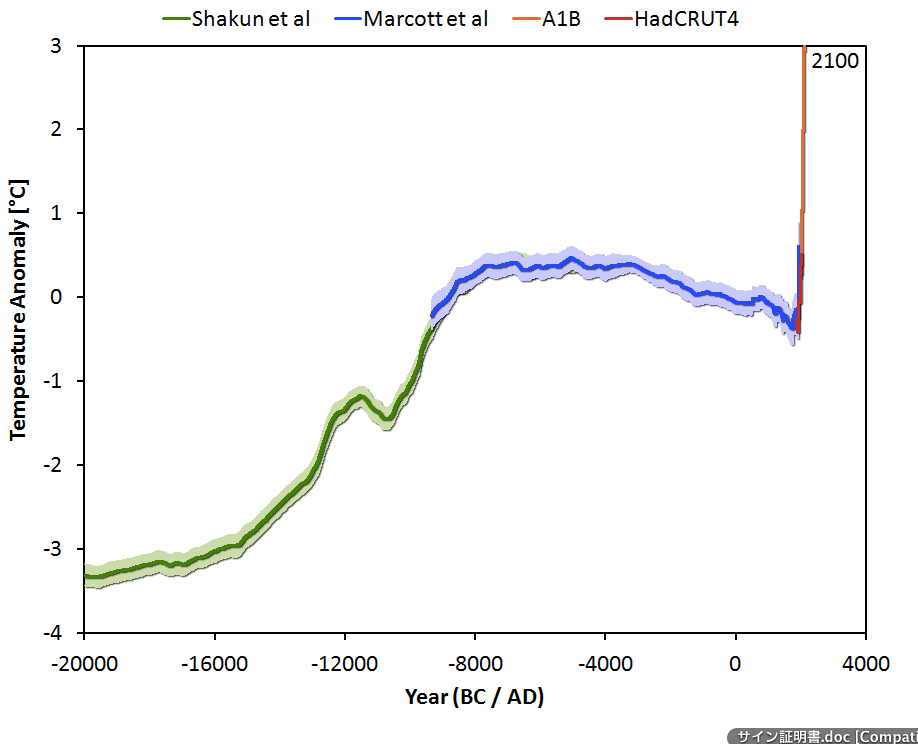

This applies to absolutely every single economic, financial and social relationship that has been forged in the modern era. The climate is undergoing a step change away from that of the holocene—under which civilisation was founded, took root and spread—to the human-generated climate of the anthropocene. The chart below, from Bart Verheggen’s blog, shows predicted temperature change set against the background of the temperature of the last 20,000 years (back to the last ice age). Message for flood prone home owners: you ain’t seen nothing yet.

Can we put some numbers on the bad stuff that could happen to the price of flood-prone houses going forward? Well the Adam Smith Research Foundation certainly doesn’t. I would sum up their paper with these words: “we used to know some stuff about the value of houses after flooding but now we don’t—and what we know we don’t know isn’t good”.

One other thing we do know is that when insurance companies know something they don’t know they will either not insure, or alternatively only insure at vast cost. Personally, when it comes to flood risk, I don’t like the fact that I know I don’t know. So when buying a house, my first reaction on coming across the merest whiff of flood risk in this new era of the anthropocene would be ‘don’t buy’. For an existing owner, the same applies: which means ‘sell’.

Finally, for those who love their houses—even if they are categorised as ‘significant’ risk—and wish to hand them down to their children, my advice would be to get active in lobbying the government to do more to prevent climate change. If you think that climate change doesn’t exist or is not your problem, then you must understand that Mr. Market disagrees.

Thank you for that excellent and well-researched pice. I came across it while googling for information as we are in the process of buying a house and trying to make decisions. We have rented next door to the house we are buying for 10 years. When it came on the market we jumped at it – it has a fantastic huge cottage/wild garden at the back and we love the location. So when it was flagged as a flood risk we were’nt too bothered initially – yes the road name is ‘Bridge End’ and yes it is 25 metres from a river, but the river is about 6 metres down and we have been told by all the locals that reservoirs built in the 1970s prevent it flooding. But then we can’t get Insurance. The postcode is black-listed – every single high street Insurer turns it down flat. Agent suggests taking over seller’s insurance. Sellers inherited the property which is empty and they only have cover for an empty property and no flood cover – seems they had to change Insurers in June. We call seller’s insurer who are a specialist Insurer and they offer cover but no flood cover. To cut a long story short I decided that it was too much of a risk (premiums could go up, cover could be pulled) unless we could get three quotes. I now have three quotes. One through a broker with a company we have never heard of, one with a reputable Insurer who say they would have turned it down flat and it was a special consideration because we are long-term members with other Insurance with them – and one from the only High Street Building Society Insurer who did not turn it down flat, but quoted £2,500 per annum. Another well-known Insurer did not turn it down flat but said they ‘may’ consider it if we had a flood risk assessment report done. Meanwhile I had got an ‘Insurance Related Letter’ from the Environment Agency (as advised on a government website) which was fairly favourable and said it was between 1/100 and 1/1000 risk. We sent it to well-known Insurer who replied that they had no reassessed our flood risk and would quote and gave us the number to call. On calling the number we were told the quote was £13,000 a year but since they now had the letter they would adjust the quote and sent the details to their pricing department – but basically they just haven’t given an answer in over a month.

So – here we are. What to do. This week I phoned the environment agency to speak to an expert and was almost reassured that it wasn’t really a risk until I mentioned all the press coverage about climate change and maybe it was a load of rubbish as we have had drought years as well. He then informed me they had done a model on climate change and predicted 30% increased rainfall in the next 100 years. We sat down and thrashed out the information trying to make conclusions from the figures and got nowhere. Common sense says – don’t buy a house near a river. But it has not flooded since 1880 before the reservoirs were built and properties that are not in a flood risk area did flood during heavy rainfall. Also the river was at its highest ever recorded level about 10 months ago – 3.19 metres – still 3 metres below us but …..

I sat down again and thought – we have 3 Insurance quotes – one is ok and there are two fallbacks. It might never flood, we can go back and ask for a significant reduction in price and install flood protection measures. However there is a limit to the flood protection measures we could install – door barriers at most – which means it depends how high a flood is – and we couldn’t protect the rear of the property against flood if it came through someone else’s back garden. Then I found a newspaper article from 1930 describing how a freak storm caused a beck 7 miles away to break its banks and come rushing downhill to our village and the river which undermined the river banks road and flooded some houses. No further information to be found about this beck – it is not shown as a risk on environment agency map.

So all in all it looks like no go – except there are a lot of people who have lived along this road all their lives, generations of them.

We really don’t know what to do! We waited a long time for a property to come up we could a) afford (it needs some renovating which we have budgeted for) and b) without moving miles away – there is very little for sale here. Also I reckon if global warming does cause more heavy downfalls of rain many places round here would be at risk of flooding. This rural area has a major river, hills and troughs, lots of little brooks and streams and of course if the reservoir couldn’t cope it would be armageddon!

We have flip-flopped for days about whether to pull out or go ahead and are praying for one little miracle thing to help us tip the balance one way or the other.

Apologies for typos

Finally – there is the Flood Re scheme due to come in next June which ‘may’ give us more Insurance options. Or it may not happen – there’s a General Election due in May.

Eleanor

This is a very complex situation and obviously I don’t know the details of your particular case. However, these are a few of my thoughts.

1. Flood Re should reduce your risk of purchase considerably. As it stands, the exceptions for residential property appear relatively minor (presuming the intended purchase is not in band H)

2. Flood Re is not open ended. It will run for 25 years. As climate change marches on and flood risk increases, neither the private sector nor the public sector will be able to afford to insure properties that are flooded regularly. The market won’t wait 25 years to factor this into the value of property: it will discount the risk that Food Re will eventually get pulled well before.

3. Even if there is insurance in place, flooding causes a massive lifestyle disruption.

4. That said, your comment suggests that we would need to see what once would be called a 1 in a 1000 year event to get to your height; of course, this number is coming down decade by decade but it sounds like there is little near-term risk of flood. Moreover, few in the UK are proactive in flood defences. I am astounded that houses next to the Thames where I live have got flooded over the last few years when even simple defences would have kept the water out. I would again look at this in terms of your ability to bear risk. Do you have sufficient funds to plan and finance flood defence well ahead.

5. Think of the flood risk for the area holistically. One of my posts refers to a Glasgow University paper that talks about “The Fallacy of Isolated Impacts”. So even if you remain dry, can you access the property by car? Will local shops and facilities get flooded? If your surrounding area gets repeatedly flooded, the value of all properties in the area, flooded or not, will fall.

6. Does the price of the property already reflect the fact that insurers are unwilling to extend cover? If so, then the trade off may be acceptable: you are taking on a property that is higher risk, but in exchange get a higher return in terms of what your money buys.

7. Finally, and probably most importantly, how does the risk of purchase fit in with your general financial situation and that of your children (if you have any). This is vital. If you are middle aged, with stable jobs, defined benefit pensions and some ISA savings, then you are well positioned if the value of the house falls substantially in, say, 25 years time. In short, if you get the house at a good price, you are in a position to shoulder the long-term risk. However, if your employment situation is less stable and your pensions are defined contribution, you may struggle to build up enough pension. Millions of people are in this position in the UK, but many have the back-stop of taking equity out their houses through downsizing or equity release to buttress a pension. If your house starts to get flooded in 25 years time, you may suddenly find that the back-stop to all your finances is plummeting in value. Similarly, if you have kids and they are not on fast track careers, the bank of mum and dad is what will get them on the housing ladder. But if your house if falling in value due to flooding just at the time they would appreciate some financial help, you will just have to say ‘no’.

So in conclusion, the stance of the insurers suggests that you are looking at a house which is higher risk than the norm. To take on that higher risk you need two things: 1) a cheap purchase price to compensate for the risk and 2) a degree of current and future financial security that allows you to bear the risk. If you see yourselves stretched financially now and for the foreseeable future, then taking on a risky asset such as an at flood risk house is unwise.

Thank you so much for that reply and apologies for taking so long to respond – I thought if there was a reply I would get an email, but just checked back on the site today. You make a very good point about future pension funding. That had slipped my mind with everything else – yes I was seeing house equity as a possible means of pension boosting in the future. Having said that, we need a home and are struggling to find something affordable. We are the wrong side of middle age and nearing retirement age with very little pension, so location was important (ie walking distance from shops and public transport), as was getting something at a good price. I could forget the pension issue, and even the location issue (there are ways round things), but it is very helpful to know that the flood re scheme has a lifespan. We have had more toing and froing and have now ruled out some potential risks. Flooding from the back is not an issue – there was a freak flood in 1930 from a beck 7 miles away, but since then the area in between has been built up. We feel the river is so far below it will never come up high enough to flood, but yes if we went ahead it would be on the basis of reduced purchase price and would look at flood barriers for entrance path and doors, as a precaution, just in case. This would sort a minor flood. If there was a major flood the whole area is likely to be affected, but our house more than some. We felt flood re will almost certainly go ahead, from reading reports, meaning the slight risk would at least be covered by Insurance if it ever happened and property would remain Insurable.

So that then left us with – ok – is it worth a slight risk. I am inclined to think not, but we can’t find anywhere else, there is very little up for sale in the area and particularly at the low end of the market, and have to move out of our current accommodation by March and can’t afford to rent anywhere (currently paying peanuts as a ‘favour’). But that doesn’t seem to me, to be a reason to buy a house just because it is on the verge of going through, if it is a risk to our future. The pension issue is slightly less of an issue, because anything else we could afford is unlikely to go up in value either due to size or location (there is only so much a house is worth however much you spend on it). We were weighing up the ‘house for life’ situation with the future profit situation.

But I do think Insurance is the key. It would be a risk to go ahead now with more expensive Insurance and then find that flood re does not go ahead as planned. We will probably still be alive in 25 years assuming the scheme lasts that long. So I guess all the indicators are it is a no go. But whenever we get to that point we feel we are just over-thinking everything and should just get on with it! A friend of ours in the business recently said he thought the future rainfall predictions due to global warming were all flawed as they had missed taking some aspect (I forget what) into consideration. But that is not very concrete really. I guess ultimately we are not going to get ;’concrete’.

But I am also aware of the wise comment about psychology you mentioned above, that people often ignore big risks as a kind of denial if they seem distant or global.

I really appreciate you replying, thank you. We are fed up of trying to make this decision! Will let you know!

With regard to the risk numbers you mentioned. The Environment Agency say it is between 1/100 and 1/1000 risk. Their letter classes it as “Medium – The chance of flooding is less than 1 in 30 (3.3%) but greater than or equal to 1 in 100 (1%) chance in any given year”. I don’t completely understand this. How can it be 1 in 100 chance if the risk of flooding is less than 1 in 30? The floor level of the house is at least 6 metres above normal river level, so about 7.5 metres above river bed. There is a wall between the houses and the river but it wouldn’t be much of a defence because there is a gate in it with steps down, almost opposite the house. There are no further flood defences planned and when I asked the Environment Agency about this – ie I asked – presumably if you thought it was going to flood here you would plan to increase the defences on that road – the answer was it was about cost per head, so unlikely. Which was not particularly reassuring.

I am coming to the conclusion that it is a no go. We have seen another house in price range (not in a flood risk zone). Smaller but better option overall. Problem is, it is with the same agent. So knowing estate agents they would probably sell it to someone else if we pull out of current one. Your info has been really helpful, thank you. I keep hanging on for this one as we haven’t really had any other options and need to move in somewhere before March. I feel the risk is small and we could prepare some flood defences. However the fact that flood re is not permanent legislation, but a scheme that could run out or be pulled at some point does make it a high risk for Insurance, saleability and future value. I could balance the last two with the need for a long term home. But the ongoing risk of Insurance being pulled or going up would not be good. Looks like it is back to the drawing board and it is very frustrating! That houses should be at risk of being uninsurable. I am still gob-smacked!

Just to let you know we pulled out of the house purchase, and I feel it was the right decision. There are quite a few properties for sale on the same road now and none are selling. Thank you for helping me make an informed decision. Had an offer accepted on something else and it is not in a flood risk zone! But does have a dodgy roof!

Easier to fix a dodgy roof than a flooded house though.

I think a wise decision. Flood prone houses are best for the deep-pocketed and those with lots of time on their hands who can make the necessary preparations well in advance. For the majority who are both cash and time constrained in their lives, the risk is too high.

Nice report. Thank you.