Last weekend, I posted a link to a speech given by Fed Governor Ben Bernanke entitled “Economic Prospect for the Long Term”. The speech is interesting because Bernanke rarely touches on the topic of long-term growth, but on this occasion he addressed the fears of many young graduates (at least those graduates of a reflective disposition) that they face a difficult future:

Now here’s a question–in fact, a key question, I imagine, from your perspective. What does the future hold for the working lives of today’s graduates? The economic implications of the first two waves of innovation, from the steam engine to the Boeing 747, were enormous…..

…… some knowledgeable observers have recently made the case that the IT revolution, as important as it surely is, likely will not generate the transformative economic effects that flowed from the earlier technological revolutions. As a result, these observers argue, economic growth and change in coming decades likely will be noticeably slower than the pace to which Americans have become accustomed. Such an outcome would have important social and political–as well as economic–consequences for our country and the world.

To counter this rational pessimism (which this blog espouses), Bernanke gave three main counter arguments.

- We can’t predict the technological future

- The IT revolution has barely started and its best fruit, in terms of economic growth, may yet to be harvested

- Globalisation allows the generation, transmission and adaption of new ideas to take place on an unprecedented scale

The only problem with this rose-tinted spectacle view of the world is that it flies in the face of the market’s own evidence. In a speech just two months earlier, Bernanke tackled the question of why interest rates were so low. The collapse of nominal interest rates is visible everywhere, as one of the charts accompanying his speech shows (click for larger image):

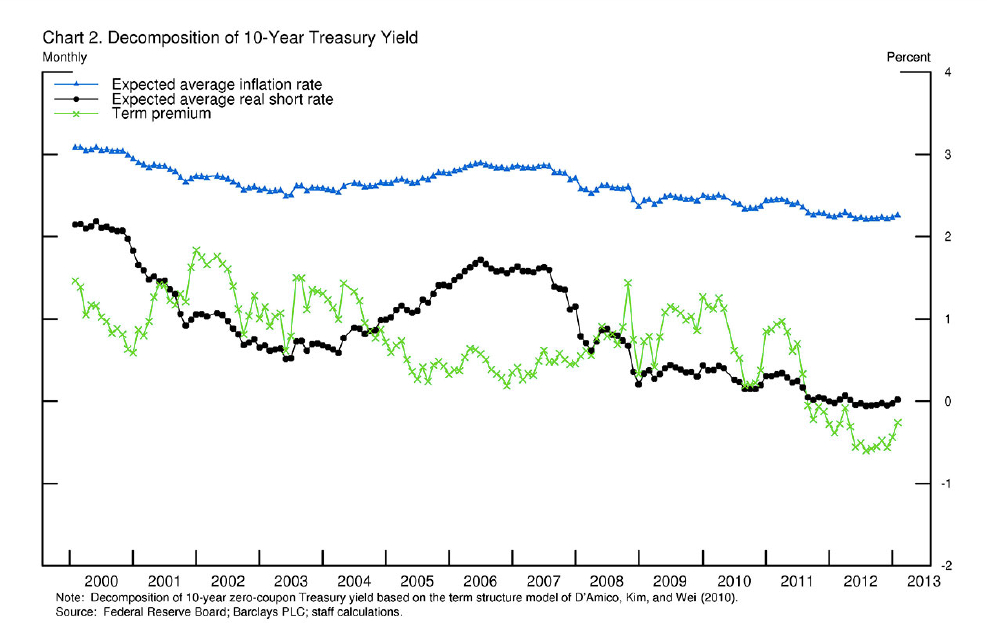

Bernanke then described a nominal interest rate as being composed of three components: a) expected inflation, b) expected short-term real interest rates and c) the term premium (risk associated with a longer maturity bond). A chart from his speech disaggregating the U.S. nominal rate into these three components can be seen here (click for larger image):

Note that the expected average short-term real interest rate has come down from around 2% in the year 2000 to essentially zero now. And what does this mean in economic terms. Bernanke provides the answer:

In the longer term, real interest rates are determined primarily by nonmonetary factors, such as the expected return to capital investments, which in turn is closely related to the underlying strength of the economy. The fact that market yields currently incorporate an expectation of very low short-term real interest rates over the next 10 years suggests that market participants anticipate persistently slow growth and, consequently, low real returns to investment. In other words, the low level of expected real short rates may reflect not only investor expectations for a slow cyclical recovery but also some downgrading of longer-term growth prospects.

The disjoint between the two speeches is obvious. In the first, Bernanke’s message—when talking to a class of fresh-faced new graduates—is a relatively upbeat one: don’t give up on growth. In the second, a speech given at a macroeconomic conference, Bernanke suggests that the market is signalling that we have a growth problem.

This also has huge implications for fiscal and monetary policy. If growth has slowed in recent years due to underlying technological factors and not just due to the credit crisis, then it will be exceedingly difficult to kick start the economy through unconventional monetary policy and aggressive fiscal injections. The policy of quantitative easing, which monetary authorities are pursuing in most advanced countries, is premised on the idea that there exists a gap between what the economy could be producing and what it is actually producing (the so called output gap). Should that gap prove a mirage then current policies will be ineffectual.

Can you call the three “counterarguments” Bernanke gave arguments at all? Especially the first two – “we don’t know the future, so it is rational to assume that it will look good”. This is silly, a classic turkey-on-Thanksgiving reasoning. Or, in other words, this is cornucopianism in its purest form.

I would entirely agree. In fact, the references he gives for the cornucopian view are surprisingly thin. I think, in general, the long-term determinants of growth are one of the weakest areas of modern economics. And note I didn’t really address the constraint to growth from resource depletion in my post.

Bernanke, like Paul Krugman, does, however, seem to genuinely believe that there is an output gap that can be closed by a combination of unconventional monetary policy and more aggressive fiscal policy. The idea is that all economies (whether in the U.S., Europe or Japan) can be knocked back onto a growth path as long as you boost effective demand sufficiently. The source of demand is almost irrelevant.

Personally, while I think there perhaps may be some potential for a short-term uplift, our problems are much more deeply seated (and please note I am not an ‘austerian’). Jeffrey Sachs did a very good critique recently of such crude Keynesianisn. His key point is that the source of the boost to effective demand does matter.

http://www.huffingtonpost.com/jeffrey-sachs/professor-krugman-and-cru_b_2845773.html

One of Sachs’ recommendations is for a very aggressive renewables roll out. I think this is spot on. Such a policy provides a classic Keynesian stimulus but also reduces an energy constraint and helps tackle climate change. It also helps increase resilience at both the national and local level. It is depressing that so many right-of-centre political groups, like UKIP in the UK or the Tea Party in the U.S., are against renewables when they make sense even taken in a purely populist light. I guess that is the influence of Big Carbon lobbying.