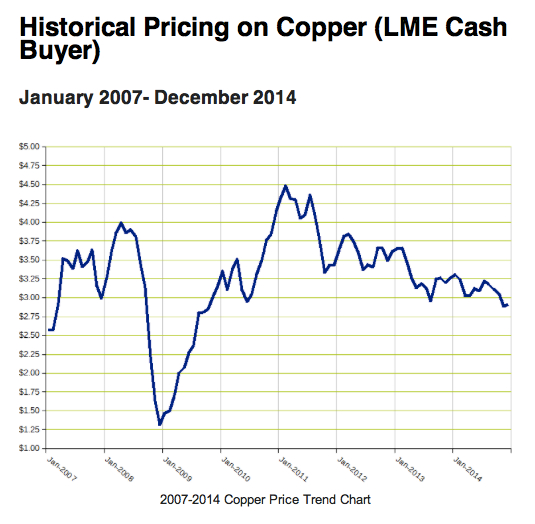

Many have been transfixed by the collapse in the price of oil, but that downturn has been paced by what is going on with copper and iron ore. Note: you can’t frack for copper (click for larger image):

And since the beginning of January, things have speeded up:

In market lore, copper is dubbed the metal with a Phd in economics due its reputed ability to portend the coming of recessions. But given China’s outsized role in providing almost all incremental demand for the commodity complex, is Dr Copper just signalling a hard-landing in China?

One observer who flagged this development well in advance is Michael Pettis, a professor of finance who blogs at China Financial Markets. Pettis wrote a piece entitled “By 2015 Hard Commodity Prices Will Have Collapsed” in September 2012 (here), in which he gave four reasons for his forecast:

- Supply was being massively ramped up, but with a substantial lag relative to demand

- The incremental increase in demand was almost all from China

- The Chinese growth model is severely imbalanced, being overly fixed investment, and so commodity, intensive

- Chinese inventories have also spiralled out of control

Pettis has long argued that countries that maintain repressive, or skewed, financial regimes that over-emphasise investment always hit a brick wall. Prime exhibits for this thesis are the Soviet Union and Japan. Moreover, the longer you pump up growth with state-directed credit, the more bone-crunching the final adjustment will be. This is what he said back in 2012:

The consensus on expected economic growth among Chinese and foreign economist living in China has already declined sharply in the past few years. From 8-10% just two years ago, the consensus for average growth rates in China over the next decade has dropped to 5-7%. But the historical precedents suggest we should be wary even of these lower estimates. Throughout the last 100 years countries that have enjoyed investment-driven growth miracles have always had much more difficult adjustments than even the greatest skeptics had predicted.

And further on in the article:

The current consensus for Chinese growth over the next decade is almost certainly too high. Even if Beijing is able to keep household income growing at the same pace it has grown during the past decade, when Chinese and global conditions were as good as they ever could be, it will prove almost impossible for the economy to rebalance at average GDP growth rates over the next decade of much above 3 percent.

Moving closer to the present day, Pettis published a thoughtful piece last month titled “How might a China slowdown affect the world?”. In the post he restates his China hard-landing scenario–nothing new there. However, he goes on to question the common description of China as the world’s ‘growth engine’.

For him, while this characterisation may be true when disaggregating the main contributors to global GDP growth, it does not correctly describe China’s role in stimulating growth in other economies. Indeed, China is more a deflationary force at present, since the suppression of consumption and the continued expansion of production have led to successive current account surpluses and a surfeit of savings seeking a home abroad.

Should the descent from GDP growth rates of 10% plus down to 3 or 4% within a decade take place in an orderly manner, it is possible that the economy could rebalance, consumption pick up and savings fall. The net effect would be mildly positive for the global economy. Should a hard landing be accompanied by chaos in the credit markets, you could see households actually increase savings and the authorities crash the yuan in a desperate attempt to use export demand to absorb excess capacity. China would then transform from being a minor deflationary influence to become a deflation monster. Nonetheless, Pettis errs on the side of optimism:

A slowing Chinese economy might be good or bad for the world, depending on how it affects the relationship between domestic savings and domestic investment, and this itself depends on whether Beijing drives the rebalancing process in an orderly way or is forced into a disorderly rebalancing by excess debt. My best guess is that Beijing will drive an orderly rebalancing of the Chinese economy, even as it drives growth rates down to levels that most analysts would find unexpectedly low, and this will be net positive for the global economy.

I am not so sure.

For the past few years I have glanced at the economic stats in the back pages of the Economist magazine. It always was interesting to me that in spite of China’s being the “workshop of the world”, Germany always had a current account surplus as large or larger than China. Considering the smaller size of the German economy, this was always a fascinating statistic.

I wonder; why do people focus so much on China’s exports when Germany is an equivalent export machine?

Joe.Yes, Germany is exporting deflation to the world, even more so now Eurozone QE will trash the euro. I think this will come into focus more as the US economy faces greater headwinds with the entire rest of the world devaluing against it.