A few posts ago, I looked at the reasons why we buy a car and highlighted mobility, aesthetics and status-signalling as key factors. Those are the ‘wants’ in the purchase decision. But the purchase decision is also determined by ‘constraints’, the most important of which is cost. At the time of purchase, we have a current budget constraint, which is the sum of money available to buy a car, and a future budget constraint which is the sum of money we have available to fuel it, maintain it and, ultimately, replace it as it wears out.

I also stated that for Tony Seba to achieve the penetration rates shown in the chart below (culminating in 95% of auto sales being electric vehicle, EV, by 2030), the EV must match or excel the internal combustion engine (ICE) vehicle in every category of ‘wants’ or ‘constraints’. In this post, I am going to focus on an auto buyer’s current budget constraint: price. So if you have a choice between buying an EV or an ICE and the EV matches or exceeds the ICE in mobility provision, aesthetic, status signalling, fuel costs, maintenance and depreciation, you almost definitely will buy that EV if it also matches the ICE in price.

This post in some ways mirrors the previous one as, in effect, we are comparing the EV powertrain plus battery against the ICE vehicle powertrain plus fuel tank. Previously, the comparison was mostly with respect to weight, but also considered volume. This time we are focussed on cost. Note, however, that for all those parts of the car that don’t relate to the powertrain or energy source, we should have near parity. True, the structural integrity of an EV must be designed to protect the battery and this may uplift costs. But, similarly, the cradling of a large internal combustion engine at the front or back of a car will also pose challenges for a designer and have its own expense. For the sake of simplicity, I am viewing those EV versus ICE costs as a wash. So really this is a competition between a battery plus electric motor and a internal combustion engine plus all its complementary parts including the fuel tank.

Let us start with the most expensive component within the EV: the battery. Again, we have to very careful over what we are comparing here: the battery cell, battery panel or battery pack? I prefer to focus on the ‘all in’ battery pack cost, which includes the heat regulating materials, battery management control panel, ancillary wiring and everything else that is required to connect the battery cells to the electric motor. As stated before, the battery pack size is determined by the number of kilowatt hours (kWh) of energy that can be stored.

In a prior post, I speculated that to almost completely eliminate range anxiety, our next generation EV would need to increase its range from the current Tesla Model 3’s 310 miles to around 450 miles. Note again that I am talking here about an EV range that will in effect eliminate range anxiety for almost all drivers, so allowing new sales of EVs to reach a penetration rate of 95% by 2030. Most drivers will likely be happy with any range north of 300 miles, but this series of posts is setting a much stricter criteria of not ‘most’ drivers but ‘nearly all’ drivers.

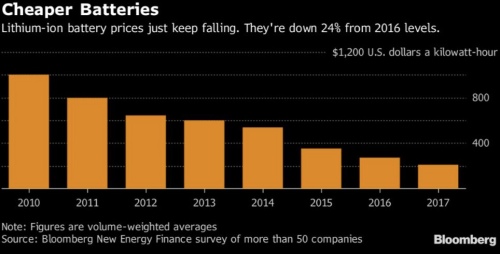

We are now ready to start applying some numbers. Let us start with the average battery pack cost per kWh. The most authoritative figure for this cost is provided courtesy of Bloomberg New Energy Finance (BNEF)’s annual survey of battery pack costs. At the end of 2017, this figure had fallen to $209 per kWh.

In my last post, I suggested that in order to get an initial range of 450 miles, a 109 kWh battery would be required. At $209 per kWh, a 109 kWh battery pack would cost $22,781. That is a lot of money for just one component of a car. BNEF analyst James Frith predicts, however, that battery pack costs will fall to $100 or below by 2025. At that price, a 109 kWh battery will cost $10,900. What does that look like as percentage of the total cost of a car?

Although China has overtaken the US as the largest market globally for new car sales, I am just going to run the numbers for US auto sales since granular data is unavailable for China. According to the Kelly Blue Book, the average cost of a new car in the United States was $36,113 as of end 2017.

So a 109 kWh battery is 30% of the price of the average new car sold in the USA. To give us some further perspective, Tesla aims to sell an entry level Model 3 with a 50kWh battery at a price of $35,000. At a cost of $100 per kWh, the battery in that particular Tesla would be around 14% of the cost of the car (and we haven’t added in the electric motor yet). How do these numbers compare with an ICE powertrain? Let us drill down into the cost of a car a bit further.

From the average new automobile transaction price of $36,113, we need to subtract dealer gross margins on new car sales. These average around 6% (source: here). Accordingly, the manufacturer’s average auto sales price pre dealer mark-up comes in at roughly $34,000.

Next, we need to subtract the manufacturers operating profits to get the cost to manufacture a car. PWC has the average operating profits at the manufacturers at around 6%. Subtracting these margins, the average cost to manufacture an average car comes down to around $32,000.

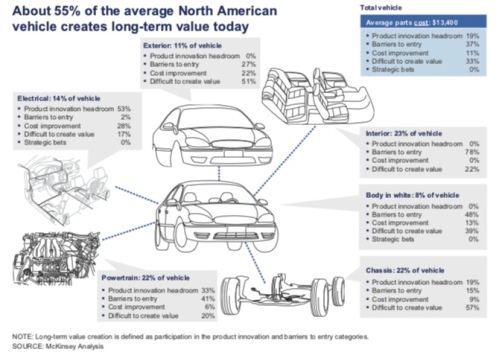

Surprisingly, I really struggled to find a good breakdown of physical materials and components as a percentage of the cost of a car. The best I could find is the chart below.

Forty-seven percent of the post dealer and manufacturer profit figure of $32,000 gives a rough figure of $15,000 for the physical material that makes up a car. A 2012 report by McKinsey that forecasts through to 2020 suggests that this figure of $15,000 is about right. In the graph below, the total vehicle parts cost given by McKinsey is $13,400. That, however, is for 2012.

Assuming the percentage breakdown of different categories of parts is the same now as 2012, we can see that the internal combustion engine powertrain accounts for 22% of total parts, or $3,300 out of $15,000. I’m going to add on to that $100 for the fuel tank to give a total of $3,400 for powertrain plus fuel source.

Following this line of thought, we next need to price an electric motor, the principal powertrain of an EV. That task is even more difficult as the manufacturers appear loathe to disclose any pricing information on the two main EV drivetrain technologies: AC induction motors or permanent magnet motors. We do know, however, that the number of components that go into these motors is vastly fewer than go into an internal combustion engine. Further, an EV powertrain does not need a gear box, exhaust system and so on. As a heroic assumption, I will assume that the EV drive train costs a little less than one third of the ICE drive train, or $1,000.

With all these numbers, we are now in a position to compare an ICE powertrain plus fuel tank with an EV powertrain plus battery. The former costs $3,400 now against a 109kWh EV power train plus battery costing $11,900 in 2025. That suggests that a mid market EV with a long range will still sell at a 25% premium to its ICE counterpart even after battery pack prices have halved. And to repeat again, for EVs to do to ICE vehicles what digital cameras did to film cameras, EVs need to either match or exceed the old technology in every category of consumer preference. A 25% price premium is not matching.

Nonetheless, all is not lost for Tony’s 2030 prediction of total dominance of EVs over ICE vehicles by 2030. First, the application of lighter weight materials in car manufacturing should allow auto makers to eke out more miles per kWh, so allowing a smaller battery. Second, more dynamic charging methods could also permit ‘on the go’ charging tops-ups that would also allow the battery size to shrink. Third, 2025 is not 2030, so the battery price will have further to fall. Fourth, the Bloomberg prediction of $100 per kWh for the battery pack price in 2025 relates to a waited average price across all EV makers. Market leader Tesla is looking at a battery pack price of $100 per kWh by 2020, giving that firm another 10 years of falling battery costs before the 2030 prediction deadline arrives.

In my next and penultimate post of this series I will look at the question of how low battery prices could go and whether dynamic charging developments could allow EVs to get away with smaller batteries yet still banish range anxiety.

For those of you coming to this series of posts midway, here is a link to the beginning of the series.

That was a long break, I was getting anxious for a while there 🙂

One thought I had was about digital cameras. I have no figures on this whatsoever but my feeling is that mass adoption started to happen way before they could match normal film cameras, because they offered other advantages such as print at home, much higher storage, and just the fact that many people love new gadgets to play with/brag about.

I am thinking about anything under say 3MP cameras, maybe even higher, they were just not actually very good quality compared to film cameras. I got a 1MP camera as my first DC and it was not great, it cost me around £100 but was not as good quality as literally a £10 film camera. And millions of these types of DC were sold. Yes, to truly kill off the film camera they had to reach parity but I think even way before that we were already quite high up the S-Curve.

I guess a car is a much bigger investment so people are going to be more price sensitive, but seeing as most people do cars and especially new cars on leasing/finance nowadays anyway, I don’t think the initial cost is going to matter quite so much as you are projecting.

It’s also then easier for people to turn this into a monthly cost to run i.e:

£300/month for ICE car + £100/month for fuel

vs

£375/month for EV + £25 for electricity

That’s already price parity and it’s 25% more expensive on the leasing/finance cost.

That’s before we’ve even considered the ongoing maintenance which is much cheaper. Once a few more people get these things and start bragging to their friends about how cheap they are to maintain, the word of mouth snowball will start to roll and we’ll start ramping up that S-Curve. All IMHO of course 🙂

I watched the hour long presentation by Seba and was very impressed, the only thing I am unsure of is that we’ll need 10% of cars on the road today because of AVs. That sounds fantastic but I just think people like having a car, and if they can afford it they’ll happily just pay a bit extra for the convenience. I am not saying AVs won’t happen and won’t make “public transport” as it were massively cheaper and more convenient for many people who never wanted to drive/couldn’t afford to run a car in the first place, but I mean… what else are relatively rich people going to spend their hard earned money on? It will take far longer than 10 years to get the car owning culture out of our… well… culture.

Cheers!

Firestarter. I would agree with you that we can get quite far up the S-curve if we relax my condition that EVs must match or exceed ICE vehicles in every category. I chose that very strict condition because I wanted something nice and concrete to test Tony Seba’s prediction that EVs would, in effect, eliminate ICE car sales by 2030.

I also think that the ‘match or exceed’ condition is really interesting in terms of whether it is technologically or financially feasible.

When we get to my last post in this series, I intend to go back and compare the competition forecasts for EV penetration. It is fascinating that Tony’s view is such an outlier: other forecasts see EV penetration at 40% or below going out to 2030, and even 2040. To me (spoiler alert) Tony may miss his number, but if he does it will only be by a bit or only by a few years. Regardless, when we do fulfil the ‘match or exceed’ condition, or even get close to it, the idea that EV penetration could possibly be below 40% looks absurd. As absurd as someone buying a film camera today (and yes there will always be arty or hipster types who love the romance of the dark room and the colour possibilities film provides, by they are very, very few).

With respect to autonomous vehicles, which occupy as much space in the Tony Seba video as EVs, I chose not to tackle that question as there was so much to talk about with respect to EVs alone. I actually agree with you in that I see car ownership lasting a lot longer than Tony does.

As I’ve talked about quite a lot, the car purchase decision is not just one of securing mobility. We buy a car for the aesthetic and for the status signalling. Dialling up an autonomous Uber provides limited opportunities for securing either. And yes you may be able to dial up an autonomous Tesla Roadster, just as some parents order a stretch limo to take their kids to a school prom, but is not quite the same as parking a Bugatti, Maserati or Ferrari on the driveway (not something that floats my boat, but for many people it obviously does). And at less exalted car-ownership heights, many people are in love with the aesthetic of the mini, or status signal with a Jag or BMW. With time, the Mini, Jag and BMW will go all electric, but I don’t think the urge to actually own one will go away any time soon.

I only started to read your article and quit when I came to a HUGE error you made. You said that Tony Seba said that 95% of passenger vehicle sales will be EV by 2030. That is NOT what Tony Seba has said. Seba has said that 95% of MILES DRIVEN will be by EV’s. That is VERY DIFFERENT.

There will be a LOT of ICE vehicles on the road still….. especially in small, sparsely populated rural areas.

Buddy. Listen to Seba from this presentation. From 26:15: “By 2025 or so, and even if I am wrong by a couple of years, by 2025 every thing that moves, road transportation, buses and tractors, and, you know, trucks and cars, every vehicle is going to be electric. Boom. Over. Every new vehicle.”

He doesn’t say that all existing vehicle will be replaced, but he does say that all ‘new’ vehicles will be EVs. So actually he is saying close to 100%. My 95% is actually, therefore, a lot lower hurdle than what Seba says. I just chose 95% because some people will choose to buy EVs just as some people choose to buy mechanical Swiss watches for aesthetic or status-signally reasons. So these posts are perfectly consistent with what Seba has said (albeit I am actually cutting his predictions quite a lot of slack since I talk about 2030 and I talk about 95% not nearly 100%).

Me again. I couldn’t resist … I had to see what other errors you made.

Here’s more BIG ONES:

1). Most people don’t have range anxiety over 300 Miles. All studies so far show that.

2). Range anxiety is NOT just about the battery size. It is also about charging stations, which are proliferating faster than rabbits.

3). Cost of battery cells is declining about 20% annually.

4). Think about this: You walk into a car dealership in 2022 and the dealer tells you that you have two choices: An EV costs slightly LESS than the comparable ICE, the EV cost of maintenance is more than 50% LESS than the cost of the ICE maintenance, the cost to RUN the EV is more than 50% less than an ICE, and charging stations are no longer an issue for most people.

What is to CONTINUE to happen, is what has already STARTED to happen: Buyers will DEMAND EV’s, and they will refuse to buy ICE vehicles. It’s alreadt started

And you haven’t even touched on autonomous vehicles, which is a HUGE part of Tony Seba’s thesis. The cost of TAAS (transportation as a service) will be so cheap …. that many people will NOT buy their own car.

Buddy

1) I don’t talk about “most people” as I make clear. Tony is talking about all EV sales so “most people” is not enough. For EV penetration to reach 95% (my lower hurdle than Seba) “nearly all people” need to have no issues over range anxiety. You miss that nuance.

2) I agree with you. Actually, I think the combination of bigger batteries, plus more charging stations plus fast charging will eliminate range anxiety. I talk about his in Post 19 of the series and will return to it in the last post 20 to come.

3) Battery costs have been declining by 20% but, as I state, you can’t just extrapolate this forward since both the battery chemistry of lithium ion and the cost of the materials will slow battery cost reductions unless we get a breakthrough in battery technology. If we get commercial solid state batteries by around 2025, then I think battery costs issues could dissolve away. But this is a big question mark and is certainly not a certainty. Battery chemistry is not subject to Moore’s Law.

4) I agree with you, but that won’t get you to a 95% tipping point. The thing about a digital camera compared with a film camera is that is outperforms on every metric. That’s what turned the camera market nearly 100% digital.

I have left out autonomous vehicles because it is almost impossible to forecast whether they will be generally available with no driver by 2030. If they are, you and Tony are right that it will change everything. But I think EVs could hit 95% of sales anyway by 2030 regardless of what trends take place with TAAS.

Overall, I think you misunderstand these posts. On a spectrum of views over what EV sales penetration will be by 2030, Seba is an extreme outlier. Even supporters of EVs like Bloomberg New Energy Finance (BNEF) are not even close to Seba (I will return to this in my last post). Over the course of the 19 posts to date, I think I have provided a lot of evidence that the eventual outcome of EV sales will actually be far closer to Seba’s view than any one else’s including BNEF (let alone the forecasts from the EIA, IEA, oil agencies and so on).

And I am putting my money where my mouth is that Seba will be more right than anyone else (although perhaps not 100% right) by investing heavily in lithium producers. I think the EV revolution is unstoppable (a rare glimmer of hope for those worried about climate change) and ICE vehicles sales will ultimately vanish even though it may perhaps take a few years longer than 2030.

…in my many years helping businesses and watching economics, it seems clear to me that the tipping point occurs when humans clearly see a cost advantage, most people are pretty astute at that… so when total cost of ownership is less for EV the ICE will fail to sell… end of an era. Exactly when we hit this I cannot know, but – anyone want to invest in a battery re-manufacturing facility?

JP