As discussed in my last post, the price of an electric vehicle (EV) battery will play a central role in determining EV sales versus internal combustion engine (ICE) vehicle sales through to Tony Seba’s forecast horizon of 2030.

In that post, I also noted that the average sales price of a vehicle in the USA was $36,113 in 2017. Further, I roughly estimated that the cost of an ICE powertrain plus fuel tank was in the order of $3,400 in that year, or roughly 9.5% of the retail sticker price for an average car. Finally, I made the heroic assumption that an EV powertrain without the battery would cost about $1,000. Accordingly, if the powertrain plus battery of an EV is to come down to the cost of an ICE powertrain plus fuel tank, then the battery most come down to $2,400. Is that possible?

To have an EV completely without range anxiety, and given current miles per kilowatt hour (kWh) of battery efficiency, I speculated in another post that a 100 kWh battery would be required. Based on these assumptions, we can back out the target price of the battery (measured per kWh) in order for EVs to match ICE vehicles in price; in other words, $2,400 divided by 100 kWh, or $24 per kWh.

As mentioned in my last post, Bloomberg New Energy Finance (BNEF) estimated that the weighted average cost of an EV battery in 2017 was $209 per kWh. BNEF analysts estimate that this number will come down to $100 by 2023 and Tesla believes that it can hit the $100 number in 2020. But how much lower that $100 per kWh can a battery pack go? Is $24 a possible 12-year target?

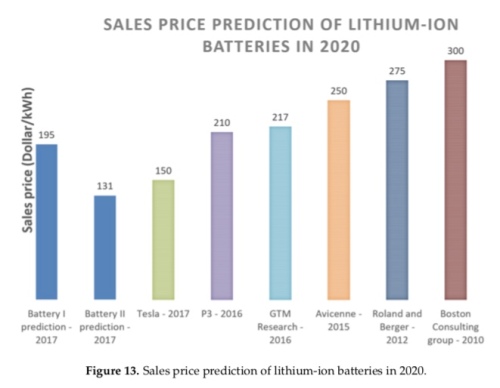

Before we get too despondent over hitting the $24 figure, it should be noted that the industry has, in general, been far too pessimist about the speed of cost reductions with respect to battery-pack pricing. The chart below was taken from a September 2017 article titled “Cost Projection of State of the Art Lithium-Ion Batteries for Electric Vehicles Up to 2030” by Berckmans et al in the academic journal Energies. As of 2018, Tesla is already well below $200 per kWh. So those past predictions have turned out far too pessimist.

Nonetheless, while Tesla/Panasonic, the market leaders in battery technology are still securing both technology-driven cost savings and economies-of-scale related cost savings, there are limits as to how far they can go in battery cost reductions.

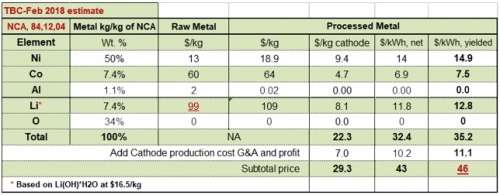

The most important limiting factor is raw material costs. The table below gives a breakdown of the cathode component alone in a battery pack as provided by Total Battery Consulting’s Dr. Menahem Anderman in a Seeking Alpha article. So the cathode materials alone come to $46 per kWh before we add in the anode, electrolyte, separator and then all the battery management software and hardware required to stop the battery overheating and to maintain the battery’s life.

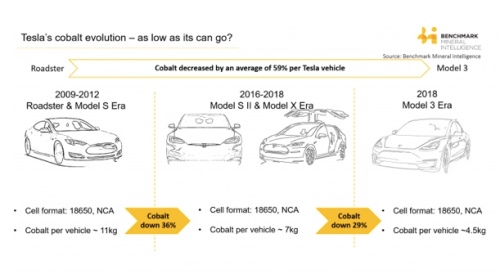

True, the most costly material used in a Tesla battery is cobalt, and the use of cobalt has been on a declining trend.

Moreover, Elon Musk made this statement in the company’s 2018 Q1 conference call (a Reuters article on this theme can be found here).

“we think we can get the cobalt to almost nothing”

Yet even if we near eliminate cobalt, the lithium and nickel alone will prevent the battery pack price getting anywhere close to $25 per kWh.

More realistically, it may be possible to achieve a $50 per kWh battery sometime after 2025. For a 100 kWh vehicle, $50 per kWh gives a total battery pack cost of $5,000, yet we are trying to seek parity with ICE vehicle pricing by producing a battery pack for around $2,500. What is to be done?

There are two possible solutions. First, a leap in battery chemistry could be achieved such that both energy density (kWh per litre) and specific energy (kWh per kg) jump higher without the need for more raw materials. Solid-state batteries appear the lead contender to become the next generation commercial battery technology some time in the mid-2020s. Apart, from eliminating cobalt, solid-state batteries would boost both energy density and specific energy and, once the technology beds down, these batteries have the potential to push battery costs much lower.

Tony Seba, however, is not looking for a technology breakthrough. A major component of Seba’s EV thesis relates to technology cost curves, and his presentations frequently feature the slide below (for example here). The curve is exponential and shows a 16% decline in costs per annum. Moreover, the technology cost curve is really an amalgam of cost-cutting achieved through economies of scale and through ‘learning by doing’. In short, these are incremental cost savings, not revolutionary cost savings.

For existing lithium ion technology, there are theoretical reasons why both energy density and specific energy cannot go above certain levels that we are fast approaching. Further, while we may be able to eliminate certain battery materials we cannot eliminate all the expensive battery materials. The only way we can stay on this 16% per annum downward-sloping exponential curve is for us to jump into a new generation of battery technology. This may, or may not, happen within Tony’s 2030 forecast horizon, but it is certainly not a given.

OK, let’s assume that we don’t get solid state out of the lab and into the factory in the forecast time horizon and we can’t get battery pack costs down to $25 per kWh. The Tony Seba thesis is that EVs will rule the world by 2030. Should we laugh at that goal? Not quite. It is possible that if we loosen our battery size condition at which range anxiety is eliminated, we may still get there. And one way this could be done is through introducing dynamic charging, or charging in motion.

Currently, the 75 kWh battery in a Model 3 can keep the car on the road for 310 miles. Accordingly, a 50 kWh battery will keep it on the road for around 200 miles. But to eliminate range anxiety, I posited in a previous post that we needed a car to go 450 miles on one charge. One way we can square this particular circle is to charge a car while it is moving, and Qualcomm is developing a dynamic vehicle electric charging (DEVC) system called Halo that does just that.

The Halo system can charge your car at a maximum rate of 22 kilowatts. Therefore, if you travelled over this system for one hour continuously you theoretically could charge your car by 22 kWh. Do that a number of times over a long distance journey, say for 3 hours in total, and that would add 66 kWhs. So now our 50 kWh EV can more than double its range to above 400 miles and bye bye range anxiety. Of course, assuming your EV driver is doing 60 miles per hour, three hours of driving translates into roughly 180 miles, or 290 kilometres. That is considerably longer than the Qualcomm 100 metre DEVC test track. And, of course, we haven’t considered the cost of the required infrastructure.

The other alternative is to bring your car to a stop, but have access to a mega super charger such that an extra 100 miles could be added in minutes. If our 50 kWh Tesla Model 3 can do around 200 miles on one charge, then to add 100 miles you would need a charger to add 25 kWh. A new charger by ABB boasts a charge rate of 350 kW. At that rate, 100 miles could be added in about 5 minutes. Such mega fast charging rates provide further challenges for battery technology, since they have the potential to severely damage a battery if not managed properly. Indeed, no existing EVs on the road could currently cope with such charge rates. Nonetheless, the next generation of high-end German EVs appear to be designed to take advantage of a new generation of super chargers, with Porsche first to market with its Mission E vehicle to be launched in late 2019. Given time, this technology is likely to trickle down to mid- and low-end EV models.

In conclusion, getting the price of a battery down to a point where EVs can blow away ICE vehicles on price is not a given. Indeed, it is very difficult to see how incremental improvements in current battery technology alone can vanquish the internal combustion engine. Nonetheless, it is just possible that the combination of a slightly smaller battery coupled with new charging technology could do the job. At that point, EVs should match or exceed ICE vehicles in every area of the car purchase decision, so setting up the possibility that the market will tip and EV domination was arrive at an unprecedented pace.

Finally, the word ‘unpredicted’ could perhaps substitute for the word ‘unprecedented’ since no mainstream organisation or company is forecasting EV sales to vanquish ICE vehicle sales by 2030. The differing EV sales scenarios will be the subject of my last post in this series.

For those of you coming to this series of posts midway, here is a link to the beginning of the series.

Reaction?

Robert. Yes, and this topic deserves a series of posts on it own. And actually the whole peak oil debate deserves a revisit. As regards shale, I do agree that low interest rates have allowed poor return-on-asset investments to be made. Investments that would have never been made in the past.

This is partly the Art Berman (http://www.artberman.com) argument that I’ve blogged on in the past. But natural gas prices have been rock bottom on the back of shale for years now while Berman was arguing years ago that we had a “Red Queen” situation given the depletion rates; that is, there existed a need to drill ever more sites to stand still with production volumes since the old ones were declining so fast. Hence, the hitting of a brick wall was inevitable.

In reality, I think the extended low natural gas pricing situation does appear to be mostly due to the fracking technology growing in sophistication rather than just a wave of crazy non-economic fracking investment.

But it could be that Berman just called the end of the fracking party two years too early. As I say, I need to revise the topic. I am not informed enough about the topic at the minute to express a sensible opinion.

Very interesting series.

You do point out that the batteries in principle allow new approaches to the design of the rest of the car. This could conceivably result in cost savings for the rest of the car, not just the drive train. Labour requirements could be lower for example, or by arranging the car geometry differently, more inside space could be had for the same amount of material, or less material for the same amount of space.

My guess is that this will allow slightly lower prices for electric cars even when the battery is somewhat more expensive than the engine.

I still think 95% by 2030 would require some moderate policy support. My own guestimate of a likely S curve includes a moderate tax on polluting cars and some subsidies. This is a continuation of what’s going on now, of course (from the 7500 Dollar tax break in the US to the various support schemes in China)

From 50% market share upwards, I also think there will be a noticeable impact on the cost of making conventional cars. Initially due to legacy overhead costs, which cannot be brought down quickly enough, and then due to evaporating economies of scale.

Heiko. You are right that the geometry of the car may differ. The push back from Bloomberg New Energy Finance against Seba though takes him to task for extrapolating the same cost decline curves for battery pricing to the pricing of the rest of the car. It’s a legitimate point: I think the fact that you have a lot more flexibility will lead to some cost savings but not double digit ones. The fact that EVs have a far more flexible “form factor” (to take the mobile phone terminology) probably adds more to the EV attractiveness in aesthetic and mobility attractiveness rather than cost saving. I am tackling the overall cost issue in my last post of the series (a post that is proving to be a long and difficult birth).

Looking forward to that.

You could also do a post on the role of policy support. I think that is one of the hardest things to predict and yet absolutely key to reaching 95% by 2030.Or maybe you can include a few paragraphs on that topic in your overall cost issues post.

I wonder what the chances are for Li-On batteries to be superseded by super capacitor Graphene batteries – which will be lighter, charge faster and last longer.

While listening to a a section from ABC Australia’s Radio National Science show titled “The graphene revolution – is it happening?” I discovered that researchers from Swinburne University’s Centre for Micro-Photonics have a graphene battery that can power a smart phone that will charge in less than a minute – last for millions of cycles – that may be on the shelves next year (see transcript below)

http://www.abc.net.au/radionational/programs/scienceshow/the-graphene-revolution-–-is-it-happening/10291372

Carl Smith: And now that they’ve made the basic prototypes, they are looking to scale up their graphene super capacitor batteries size and storage.

Han Lin: In the near future we will be able to fast-charge a cell phone in less than one minute so you can be fully charged and power our cell phones for a whole day. It can be charged and discharged really fast. It has millions of life cycles, and is environmentally friendly. In addition to that, no matter how you treat it you will not get very hot.

Carl Smith: How far off are we seeing these on shelves soon?

Baohua Jia: The prototype will be available hopefully by the middle to end of next year, and then from that point I guess it won’t be too long to allow it to be on the shelf. It’s a bit sensitive, but I’ll say that the methods that we are using actually gave us lots of advantage. We can actually achieve almost world-best performance in terms of energy density.

A few words of encouragement from me, I am still very much looking forward to your next post.

Apologies Heiko. Am working on it 🙂 I had to take 2 months out to sell my late mother’s house, which included emptying the contents and so on. This just pushed everything else in my schedule to one side, including blogging. But am back to working on a blog post now.

My condolences on your loss. When there are a lot of memories attached to the contents of a house, it can be quite a hard task.

We are at 100$ per kwh at the end of the year by TESLA. Seems somebody is again underestimating exponential functions in this article. It is funny to see that people always do the same mistakes when it comes to disruption and change.

Lars. If you read that article carefully, Musk is referring to the battery cell price price per kWh not the battery pack price per kWh. So at the pack level we are still quite some way from getting below $100 per kWh. And we need to concentrate on the pack, because it is the cost of the battery pack as a whole that currently makes EVs more expensive than ICE vehicles.

Hi,

I really enjoyed these posts, and think you did a great job drilling down on these topics. One question I have is that I don’t think Seba’s analysis focuses on share of cars as much as share of passenger miles – with ride-share via autonomous vehicles taking the lion’s share and individual passenger cars dropping significantly. Thus, the total number of cars needed to reach 95% of passenger miles is significantly less than if we kept the current configuration of multiple private cars per typical household.

Also, I wonder if you and Seba have ever considered doing a podcast or some type of interview together. I would definitely think that would be well received!

Thanks!

Herman. Thanks for the comments. I agree that the switch to autonomous driving was the second pillar of Seba’s analysis. I took a decision to leave that out since we appear to have far less visibility in terms of the technology in this domain. And, for a more practical reason, the posts on the EV topic were multiplying far beyond what I had originally envisaged even before taking on another topic.

Nonetheless, you are right that ultimately we will have fewer cars driving a lot more miles. Accordingly, at some stage total auto sales (ICE plus EV) will peak out, which will have a knock-on effect on the shape of an S curve. Whether that happens within the forecast window to 2030 I am not so sure. I would need to look at that question in a lot more depth.

Hi,

I completely agree with you that addressing autonomous vehicles at the level that you’ve taken with electronic vehicles (EV’s) would be a massive undertaking, and until I’m willing to do that myself, I can’t very well criticize you for leaving this aside for the time being. I would respectfully disagree, however, regarding the impact of this lacuna on the conclusions to be drawn from your analysis.

First let me quickly (and probably inadequately) summarize Seba’s argument. He points to three exponential disruptions occurring roughly simultaneously: EV’s, autonomous vehicles,

and business model innovation (ride share on demand). These three disruptions, Seba argues, will lead to the radical transformation of the transportation sector. Throw in his predication about solar power cost decline and you have, basically, a complete reset of the global economy.

The most obvious impact of discounting the role of autonomous vehicles and ride share is that your analysis requires us to assume a 1-1 replacement of ICE with EV’s which multiples the costs/barriers for EV adoption many times over (2x to 4x+) including: battery size/cost reduction, number of EV’s, lithium production and capital required.

More fundamentally, rather than introducing a more constrained projection than Seba’s “hyperbole,” your analysis actually seems to be arguing for a much more radical position. Something like: Even if Seba is wrong about the autonomous vehicle and business model transformations, and key costs of transitioning to EV’s are many times higher than Seba assumes, the energy and transportation sectors are still likely to experience epic disruption just based on the adoption of EV’s.

Again, thanks for the excellent posts and analysis – I really enjoyed them.

Herman. You are absolutely right that I have made the over-simplification of a one-to-one substitution between ICE vehicles and EVs. Further, if total vehicle sales peak before 2030 (the forecast period), then you are right again that the resource constraints, capital expenditure requirements for buildings factories and so on will be reduced.

Nonetheless, I am unsure as to whether the advent of Level 5 autonomous vehicles will automatically lead to a reduction of car ownership. As I talked about in my articles, we buy cars for three major reasons: 1) mobility, 2) aesthetic and 3) status signalling. EVs actually could increase the attractiveness of car ownership in many cases. Owning ICE cars is a pain in terms of running costs and maintenance, EVs not so much. Further, the aesthetic attractiveness of EVs is likely to rise rapidly. Their form factor can be far more creative than that of an ICE vehicle and they will provide a whole suite of new digital services. All are positive reasons for car ownership.

Indeed, this revolution can throw up all kinds of anomalies. For example, in the UK where I live 25% of cars are parked on the street since the owner does not have access to off-road parking. This causes a number of disincentives for car ownership: owners may be required to buy a residential parking permit or they may have to hunt around for free parking on-street spaces that may be a short walk from their home. With an autonomous vehicle, the car can just be summoned when needed from a free parking spot away from the owner’s home. We rather automatically assume that inner city dwellers will be the first to move to Transport as a Service (TaaS) models. But lots of them already operate on a TaaS basis through being reliant on public transport. Autonomous EVs could actually attract them away from public transport and into autonomous EV ownership.

We can get even more creative. An autonomous EV could be thought of as mobile extension to one’s house. You could outfit one as a home office, with a lap top, printer and so on, summon it to door and have it drive to some beauty spot where you can work on a spreadsheet or PowerPoint while taking in the view. You won’t want to do that with TaaS car since you will want to keep all your stuff in the “mobile room” and not lug it in and out of your house.

I have no idea how all these forces will offset each other, but will certainly be fun watching as it all works through.

BTW, after seeing a lecture given by Varun Sivaran at the Oxford Martin School back in June and reading his book “Taming of the Sun” I’ve been planning to tackle Seba’s renewables plus batteries revolution thesis as well. Hope to kick off that series of posts in the New Year. But if you want to see the video of Sivaran’s talk you can find it here:

https://www.oxfordmartin.ox.ac.uk/videos/view/686

And this is his book:

https://mitpress.mit.edu/books/taming-sun

Hi,

I agree with your focus on EV and Solar. Of Seba’s four hypotheses (EV, Solar, TaaS and Autonomous Vehicles), I think that EV and Solar are the ones with the greatest potential impact and also the most uncertainty.

Regardless of what happens to TaaS and Autonomous, EV adoption would lead to a displacement of the oil industry, and solar adoption would displace the coal and gas industries. Either of these developments on their own would lead to an major economic realignment and together they could transform the global economy.

The other two hypotheses are actually far enough along so that they can (for the near term future) facilitate and magnify the impact of EV and solar, even if there may be some constraints that hold up their further adoption sometime in the medium to far future.

As you point out, TaaS is not really a new innovation any more. It is in a rapid growth phase. While it could hit some economic or cultural ceiling, there doesn’t seem to be any internal constraint on its growth.

While level 5 autonomy is still being developed, level 4 (limited range fully autonomous) seems to be at an inflection point. Level 4 alone could be highly disruptive and may be able to fuel the first leg of exponential growth for autonomous vehicle (next +/-5 years). For example, public transit (buses) and long haul trucking sectors are both field testing level 4 autonomous vehicles. Rush hour commuter driving and long haul trucking are generally not seen as esthetically pleasing activities and probably have few barriers from drivers to autonomous adoption.

When level 4 adoption growth starts slowing, level 5 may or may not have been perfected which would impact the ceiling for autonomous vehicle adoption. I think it would take an analysis similar to the form that Varun Sivaran used with solar to get visibility into wether we will see a smooth level 4 to level 5 transition, but that doesn’t seem to be an immediate constraint on this technology.

Thanks for the excellent reference about Taming the Sun video/book. It should be a great counterpoint viz Seba’s predictions.

9.4% total cost of car for fuel tank and powertrain. What about the transmission? From most estimates I have seen it is more likely to be in the 20-25% range of total cost for the ICE drivetrain. Using your figures, 100kWh battery, that would put it at $80 per kWh. Tesla car batteries range from 62kWh to a 100kWh batteries, so you are calculating worst case scenario. A 62kWh battery would need to be $129 per kWh to match ICE cars.

Tesla has just dropped the price on it’s model 3 to $36200, almost the exact figure you used for your example. How long before that price drops? It has less range than an ICE car but costs less to maintain, less to fuel, has a much greater lifespan and the most important part, reduces carbon emissions.

My money is on Tony Seba.

Mark, powertrain includes transmission. I would generally agree with you that we are at the first of the tipping points. I see from EV Volumes that official plug in market penetration was 3.8% in 2018, huge jump from 2017. It’s just this is really a series of tipping points at different price points and different vehicle specs. Think the direction of travel is obvious: it’s game over already for ICE vehicles. My caveat is just that I think it still unlikely that it will be total game over by 2030 as Seba suggests (95% EV penetration a mere 11 years away). But if we get to that point in, say, 2035, Seba is basically on the side of the winning argument vis a vis the IEA, Exxon Mobile and the rest’s predictions. So my money is also on Seba, but just a few years further out.

I know I’m late to the party, but thank you for a very informative series.

A potential factor where advances in battery tech could tip the economics towards EV’s concerns battery life. If, as Musk hopes, improved manufacturing methods and tweaks to chemistry could lead to a 1 million-mile battery, that could be a game changer. Assuming an annual car mileage of 14,000 miles (current US average), that could potentially give a 1 million mile battery a 70+ year life. Even if we scale down these optimistic forecasts to a ~20 year economic life, that means (assuming a continuation of the current average car replacement period of 7 years) one battery would be able to power three successive cars (in effect). That means higher retained value, with the associated reduction in lifetime cost (running cost + depreciation). The upshot is that higher retained values give EV car companies the scope to revise their financing offers such that cost of ownership for buyers is reduced, perhaps to the point where the gap between EV’s and ICE’s reduces to nothing (or even in favour of EV’s).