Here we go. Tony Seba declares it’s “boom, over” for the internal combustion engine (ICE).

In this series of posts, I’ve tried to provide some metrics to measure whether Tony could be right. Central to my thesis is that when electric vehicles (EVs) match or exceed ICE vehicles on every criteria then “yes” it will be “boom, over”. Let’s revisit the criteria from post number 13 in this series. The sources of utility derived from a car can be thought of as threefold:

- Mobility

- Acceleration

- Top speed

- Handling

- Internal volume

- Configuration

- Off-road and specialist capabilities

- Aesthetic

- Status signalling

With respect to mobility, EVs are already superior to ICE vehicles in terms of acceleration and top speed. With their low centre of gravity (governed by the battery), their handling characteristics are also very good. Moreover, the small size of EV motors means that ultimately we can have motors front and rear, or, indeed, on each wheel. With each such modification, EV handling will pull away from that of ICE vehicles.

The powertrain of an ICE vehicle is a lot bigger volume-wise than that of an EV. It’s only through taking into account the big battery that the entire drivetrain of an EV matches, or possible exceeds, an ICE in volume. Here again, however, technology favours the EV. Batteries are getting smaller. The internal combustion engine has been around for 100 years. It won’t get much smaller. So, in time, the entire drivetrain of the EV will be smaller than that of an ICE, freeing up space in the rest of the car.

The fact that EV motors are so small and don’t require gear boxes, exhaust systems and other ancillary equipment means that they already favour creative configurations. At the minute, the size of the battery is so big that it limits flexibility provided by the smaller electric motors, even though we could chop up the battery and put it in different places. Distributing the battery around the car though is currently not an efficient thing to do since it adds complexity to the electronic control panel and heating systems regulating the battery. But as the size of individual battery cells come down, the battery can be placed within the required form factor of the overall car just as it is in a lap-tap computer. Ultimately, we will move to a designer-led car rather than an engineer-led car, as with smart phones.

With the independent control of each wheel and a freehand regarding configuration, designers can also dream up the perfect MPV, SUV or pick-up truck. Dropping the tyranny of the big engine, gear box, crankshaft, and exhaust system means that future EVs will be able to cope with challenging terrain or complex pulling and carrying requirements far better than ICE vehicles.

Now we get to aesthetic and status signalling. The rush by high-end German auto makers (such as Mercedes, BMW, Porsche and Audi) to roll out EVs in response to Tesla shows that EVs are soon going to dominate high-end auto sales. Indeed, Jaguar‘s top management is now debating whether to transform the brand into an only-EV one near term (here). The strategy of other top-end makers like Porsche is to offer a full-range of EVs alongside the old ICE vehicles. But the key point here is that all the luxury brands now see no contradiction between a car with an electric drivetrain and a car that conveys high status.

True, for those ICE aficionados, the sound of an ICE engine and the steam punk-type glory of lifting a bonnet to see a V8 will never be eclipsed by an EV. But the new Tesla Roadster will place all of these vehicles in the rear-view mirror. So there will remain an aesthetic and status-signalling rump demand for ICE vehicles, but this will be the same rump demand as exists for Swiss mechanical watches. Demand for Swiss mechanical watches exists but its irrelevant in terms of aggregate revenue for the watch industry.

But now we come to the chink in the EV armour: price. As pulled out in previous posts, affordability is a temporal constraint: it stretches from the present to the future. So the purchase decision is not just bounded by the current available budget available to buy a car now, but also by the budget you will have to run the car through time and, ultimately, replace it. Restated, the purchase decision takes into account the sticker price and future costs captured by fuel, maintenance and depreciation.

EVs are already ahead of ICE vehicles with respect to fuel costs, maintenance and depreciation. And if something costs less in the future, theoretically you should have more money to buy it now (financing and credit facilities allow one to push payments for a car from the present to the future). In other words, if we can lessen future costs, we have more money to buy a more expensive car today.

So to repeat: given EVs are superior to ICE vehicles with respect to mobility functions, and can be at least as good with respect to aesthetic and status-signalling, once their price approaches that of ICE vehicles, looked at in terms of the aggregate purchase price and future running costs, the market will tip. That is, sales of EVs will grow exponentially and ICE sales will collapse.

At this juncture, we should emphasise that the car market is not one amorphous mass. It is highly segmented with the vehicles in each space having a particular combination of mobility, aesthetic and status-signallying functions and price points. Thus, we are not really talking about a single tipping point, but a series of rolling tipping points as EVs meet the required sales take-off criteria in each segment one by one. To get a sense of the segment breakdown in the US, 2016 sales by type are given here:

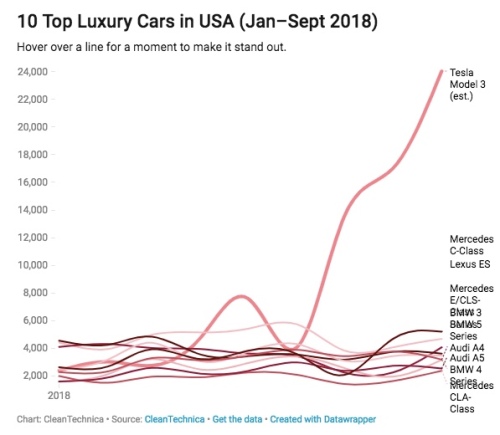

Next question: “Are EVs at the tipping point in any of the above segments?”. Twelve months ago, the answer to that question would have to be ‘no’. But you are lucky to be living at a unique point in history. As of the third quarter of 2018, the answer must be “yes”, and that is down to Elon Musk and his Model 3. The rise of Model 3 sales over the course of 2018 has been nothing short of stupendous despite all the much-reported production issues.

The Model 3 is leaving its rival brands in the dust:

The next segments up for attack by EVs are luxury mid-size and large SUVs and crossovers. Here, the incumbent brands look like they will get to market first since Tesla has its hands full fulfilling its Model 3 order book before it can move on to its crossover Model Y.

At the top end, we have the Jaguar i-Pace, soon to followed by the Audi e-Tron and the Mercedes EQC. The adage “build it and they will come” appears to be holding true again, as the i-Pace has a full order book and Jaguar has hopelessly limited capacity to meet demand. In short, we have evidence that when an EV offering is at a similar price point to incumbent ICE vehicles, you will be able to sell all the EVs that you are able to make.

To repeat: what the sales data are starting to show is that if an EV is offered at a similar price point to an ICE vehicle, the public will buy the EV since an EV is a better transport alternative in terms of performance. Basically, the meme that the pubic don’t want EVs appears total rubbish. Given this state of affairs, what are we to make of these two charts. The first is from a Citibank report on EV penetration rates, and the second from an article by David Roberts of Vox.

In the top chart, the high-end 70% sales penetration rate by 2030 forecast is predicated on a breakthrough in technology (probably a commercial solid state battery). Personally, I don’t think that will happen until a decade later, so can put that forecast aside.

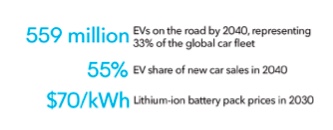

Based on lithium-ion technology, we are really looking at 2030 sales forecasts by every single forecasting entity of less than 50% of total vehicle sales. One of the most bullish forecasts is Bloomberg New Energy Finance (BNEF). This company’s latest Electric Vehicle Outlook 2018, which forecasts forward to 2040, was published in August and can be found here. The headline quote for the report:

And from inside the report a percentages sales penetration number:

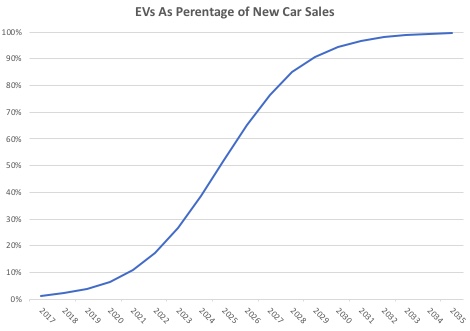

So the bullish BNEF suggests we need another 20 years at least before EVs overtake ICE vehicles in total sales. Keeping that in mind, Tony Seba’s belief that the EV sales penetrations will be over 95% in 2030 is not just an outlier compared with other forecasts but on a completely different planet (my graph based on Tony’s statements):

The disconnect is massive. In effect, BNEF, one of the most bullish mainstream forecasters of EV sales, sees a penetration rate a lot less than half of that of Tony Seba in 12 years’ time.

Nonetheless, as one of the first vindications of Tony’s theory, in the small- to mid-sized luxury car segment Tesla alone was around one third of total sales in September 2018!

Moreover, with a slew of new entrants, the luxury crossover and SUV segments is going to experience an identical attack by EVs on ICE vehicles as the cost and performance metrics are basically the same as the luxury car segment. Accordingly, the only way that BNEF and all the other companies and organisations that forecast total penetration rates well below 50% in 2030 can be right if one or both of two conditions are fulfilled:

- EVs can’t get down to cost parity in the mass market car, SUV, crossover and pick-up segments, or

- The demand exists across all segments for a Seba style 90%-plus penetration rate, but not enough batteries can be produced and/or EV production lines put in place to fulfil demand.

Now if you listen through Tony’s presentations, he claims that battery-price falls have accelerated from 14% to 20% per annum. He then projects these trends forward and sees EVs being chapter than ICE vehicles across the board in a few short years.

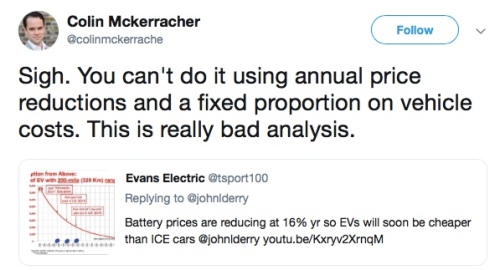

The head of BNEF‘s team Colin McKerracher has some rude things to say about this. From his Twitter account,

And in response to Seba a short Twitter spat ensued:

Mckerracher’s argument is that as the price of the battery comes down, in percentage terms it will become less dominant in the overall price of the car. I agree with this argument, but I don’t think it is enough to knock Seba’s huge EV penetration number out of the ring.

As I have argued throughout these posts, EV’s are superior to ICE vehicles in a number of domains like performance, running costs and so on. Accordingly, they don’t need to be cheaper than ICE vehicles to replace them. All they need to do is reach price parity. And we are witnessing real time what happens when EVs match ICE vehicle in a particular segment with respect to price: in the small- to mid-size US luxury car market we are seeing the market tip toward EVs in a matter of months.

In the same Twitter exchange, another poster put up a helpful chart to show the price fall dynamics of a 16% battery price decline with the price of the rest of the vehicle’s main components kept static. The battery is very much the swing component.

In my last post, I did some rough, back-of-the-envelope calculations so as to determine what the battery price needed to get down to in order for a mass market EV to sell at parity to an equivalent segment ICE vehicle. Look at the post for details, but the bottom line is that the battery needed to be produced for $2,500 for a 2017 US average sticker price model of $37,500.

From Electric Vehicle Outlook 2018, BNEF sees battery pack prices at $70 per kWh in 2030. Further, given the almost daily advances in battery charging speeds taking place at present (we seem to be on a through train from 100kW to 350kW and beyond), a mass market vehicle should be able to get away with a 50 kWh battery (which with a 350kW charging station will recharge in a little over 8 minutes, assuming that battery chemistry and control will have advanced to a stage that can cope with that speed of charge in 10 years’ time).

Seventy times 50 is $3,500 dollars. So let’s say that this makes the EV $1,000 more expensive than ICE vehicle or 2.7% more. As I mentioned above, the aggregate cost of a car is the price of purchase plus running costs. Given EV running costs are lower, a slightly higher EV sticker price of purchase is completely compatible with my concept of total cost parity.

As a reality check, even today we are seeing the first stirrings of proper EV offerings in the smaller vehicle segments. The Hyundai Kona, a small SUV, boasts a 64kWh battery and a range of around 300 miles. Just launched in the UK, it sells for around £25,000. Add back in the government subsidy of £5,000 and the total comes to £30,000 or about $40,000. By comparison, in a similar segment in the US the Honda CR-V and the Toyota RAV 4 sell for around $30,000.

Hyundai uses the LG Chemical NCM 622, which has a relatively high cobalt content compared with Tesla‘s battery. Consequently, I would guess that the Hyundai Kona battery costs around $200 per kWh, or $12,800 for the 64kWh battery overall. If we could get the kWh cost down to $70 in line with the BNEF forecast, the battery would come in at $4,420, for a saving of $8,320. At that price, the Hyundai Kona would sell for about $1,500-$2.000 more than the RAV 4 or CR-V. Basically parity given that the Kona will be cheaper to run.

True, getting the battery cost well below $100 is a challenge. There are two opposing forces we should consider in the declining battery cost trajectory. BNEF rightly point out that Tony’s per annum price decline forecasts are less useful that an experience curve approach (in economics we talk about economies of scale and learning-by-doing effects). What this means is that price declines are not a function of time but rather how many batteries you produce. Thus, if the volume of batteries produced goes up exponentially, the price of the batteries comes down exponentially.

And if you want to get a sense of how fast battery capacity is being ramped up, then you should follow this link and read the article by Simon Moores of Benchmark Mineral Intelligence. Moores notes that existing and announced battery factories will have the capacity to produce 1.1 TWhs of batteries per year. That is over a 10-fold increase over existing production. The scale of this application of capital and innovation should reap huge cost-cutting rewards.

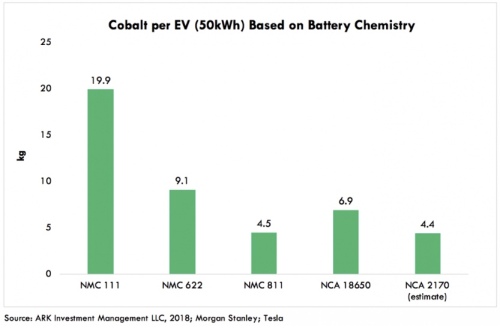

The major impediment preventing batteries costs coming down well-below BNEF‘s forecast of $70 kWh in 2030 is the price of the raw materials that go into a battery. Very roughly, 0.8kg of lithium goes into a 1 kWh battery, and that amount of lithium currently costs about $10. The most expensive metal used in current generation lithium-ion batteries is cobalt, which at one stage got as high as $90 per kg, but is now around $62. From the chart below you can see that different battery technologies use different amounts of cobalt. The NMC 811 battery, viewed as one of the most advanced battery chemistries in terms of energy density, is eight parts nickel to one part cobalt to one part manganese). A 50 kWh battery uses 4.5kg of cobalt or about 0.1kg cobalt per kWh. That is worth about $6. Nickel current trades at about $13 per kg. So for an NMC 811 battery we are looking at about $10 per kWh for the nickel. Thankfully, manganese is relatively cheap, so isn’t a big swing factor in battery pricing.

Nevertheless, if you add the three most costly metal components together, we have a floor cost of $25. And these are the raw materials for just one component in the battery: the cathode! You then need to complement the cathode with a graphite anode, an electrolyte and a separator. Then these components have to be combined into cells, which are linked into battery modules, and finally fabricated into battery packs. And the whole system requires a very sophisticated charge management and heat control system. In sum, getting battery prices below $100 per kWh with current lithium-ion technology will be tough.

With that caveat in mind, I will ask the following question to finish this series of 20 blog posts on the future of EVs:

“Is Tony Seba delusional in seeing EVs totally displace ICE vehicle sales by 2030?”.

My answer to that would have to be “no’. Ninety-five percent plus penetration is certainly a stretch goal since it would require current lithium-ion battery technology to be pushed right up against the boundary of what is possible in terms of price and performance. But I feel it is just about doable.

Does that mean that I think it will likely happen? That is a different question. I’m a probability guy and prefer thinking about the range of possible outcomes as opposed to giving one point estimate. For me, saying EV penetration will definitely be X percent in 2030 when looking at such a dynamic industry is a meaningless thing to do. My own guesstimate is that the EV penetration rate will likely be somewhere between 60-80%, which still puts me completely outside of the mainstream.

Nonetheless, in the spirit of Tony Seba hyperbole, I am happy to go out on a different type of limb. So in my words (rather than Tony Seba’s):

“All those who think EV sales penetration will remain down at around 30% in 2030 (the consensus view) are completely, utterly and certifiably crazy!”

For those of you coming to this series of posts midway, here is a link to the beginning of the series.

Very interesting, you put a lot of effort into this.

One of the issues I wonder about intensely is the impact of government policy. Now it is obvious that there is a large impact. EV sales (pure electric, September 2018) in Norway clearly are at 45% because of government policy, while they are less than 1% everywhere, where the regulatory and tax enviroment is poor.

Looking at the phase out of the tax credit, I have tried to find a suitable precedent. I have dug up the numbers for Denmark:

Tesla sales in December 2015: 1249, best selling car in the country that month, outselling all others

Tesla sales in 2018 year to date: 71, in September. 12

https://focus2move.com/danish-auto-sales/

A good summary of the tax change:

To summarise even further between 2015 and 2018 in Denmark:

Model S from 80000 to 105000 Euros

Equivalent Mercedes Benz S class from 265000 to 235000 Euros (I had to do a bit of digging to arrive at those estimates)

How does that compare to the US and Tesla?

The main support mechanisms in the US: Federal tax credit at 7500$, California credit of 2500$, ZEV credits (value more opaque, difficult to predict and the subsidy goes to the manufacturer), exemption from gasoline taxes

https://www.engadget.com/2017/04/13/california-electric-vehicle-fees-2020/

https://www.congress.gov/bill/115th-congress/senate-bill/3559/text

Overall, this looks like it is going to be a somewhat smaller hit, but not so much smaller that it is likely to be negligible. This should pull Tesla sales into the second half of 2018 and potentially create a hangover in 2019 and 2020.

I think it is hard to estimate the impact of policy and the interaction with technology development. Clearly, there is some positive feedback, as we have seen with battery pricing.

To put my guesswork into numbers (and assuming similar policies outside the United States). 95% penetration by 2030 should be doable by extending the federal tax break until 2023 for all manufacturers and only then slowly reducing it by 1500 Dollars per year. In addition, there should be a tax on conventional cars, which goes up by 2% every year. So that would be 10% in five years time, and 20% in ten years time. For political reasons I would expect that “tax” in the United States to take the shape of harsh CAFE regulations, which should have the same impact on sales prices, but be a much easier political sell.

In 2029, that would mean a conventional car that today costs 37500$ would retail for 45000$. However, with declining market share there should be diseconomies of scale, so we might actually see a price of 50000$. On the other hand, mass produced I think electric cars can be a little cheaper than conventional cars today, so we’d have a price of 35000$ and a substantially steeper difference based on total cost of ownership.

With the tax credit quickly phased out, a usage fee being introduced to compensate for the loss of gasoline taxes and no additional taxes (/harsh CAFE requirements) for conventional vehicles (and this lack of policy support applying to all major markets, not just the United States), I would not be surprised by EV share staying below 5% even in 2030.

Now, I think that the second scenario is especially unlikely. Even if there is little support in one major market, there should be sufficient support in another, and that in turn means more battery volume, therefore lower battery cost and therefore more market share than there would be otherwise even in markets with little government support.

Overall, I agree with your guestimate of 60-80% based on the likely policy mix across major markets (most favourable in China, less favourable in Europe, least favourable in North America).

Thanks Heiko. I did consider delving into the public policy issue, but the series of posts had expanded far beyond what I originally envisaged, so I decided to leave this to another time.

Thanks also for the links. I am not so sure whether credits will be a long-term swing factor. As EV penetration picks up, I think most schemes just become self-limiting as they become too costly. But they are certainly helpful for allowing EVs to reach take-off point.

Much more interesting to me is when certain cities impose outright bans on ICE vehicle access. Much of the range anxiety issue with EVs is a question of perception rather than actual practical limitation. Few people have a need to drive 200 miles without stopping. But the psychological perception that we are able to drive 200 miles without stopping is still important. Likewise, the whole idea of car ownership rests on the sense of freedom stemming from an ability to drive anywhere when you want. Should suddenly certain areas of a country become out-of-bounds to ICE vehicles, I feel this would deal a huge psychological blow. You may rarely need to travel into a city centre with an ICE ban, but when such a ban exists, the freedom to drive an ICE vehicle anywhere you want would be dramatically curtailed. Again, it’s a perception thing.

I am looking forward to your post on the public policy topic (I realize that this may not be your next post, but be a bit further out in the future). You are very thorough indeed, when you write a post..

You probably heard about the latest Republican proposal on tax credits.

https://insideevs.com/republican-extend-federal-tax-credit/

I completely agree that a phase-out of subsidies will happen in most countries, and certainly in the United States. Norway is maybe a possible exception, because the subsidy is apparently already structured as a punitive tax on ICE cars, and with a 45% EV and 15% plug-in hybrid share in September, going to 100% EV might not be that hard while simultaneously keeping the structure of the policy support basically as it is.

The design of the phase-out is clearly tricky. There are a few poorly done precedents, most notably Denmark, as I mentioned already, Hong Kong,

and the Netherlands.

Click to access Special%20elektrisch%20vervoer%20analyse%20over%202013.pdf

The last link is in Dutch, but you can figure out the tables without knowing Dutch. The incentive phase-out for plug-in hybrid vehicles led to a market share for full EV’s and plug-in hybrids of nearly 25% of the overall car market in December 2013. Most of those were plug-in hybrids.

I realize that these are all very small markets, and therefore, there was enough manufacturing capacity elsewhere to supply these spikes, and there was enough demand elsewhere that the subsequent market collapse did not matter much. They are certainly not visible in the S curve for the whole world.

Getting it right in the US I figure will matter a lot more.

The outright bans are also interesting. I think there is a bit of positive feedback there, as well. When EV market share is high and there are a lot of reasonably priced EV’s, I guess it will be a lot easier to get an outright ban in a city enacted.

Thanks so much for this, this a great break-down and analysis to Tony’s evangelism – really appreciate a thoughtful reality check

I think you are being super conservative in that EVs will have to have exact same capabilities as ICE to wipe out ICE. Long range travel may be Achilles heel for EVs for a while but look at normal driving habits. Most cars, trucks are driven what, 20-40 miles a day? With 200 mile range, staying between 10-90 percent charge, over night charging at home, every other day will do you. With Uber, easy car rental etc, filling in the gap occasionally for road trips etc, is trivial non-concern for anyone that is not on the road for work or, say every weekend for family/relationship reasons.

So you give me a EV that is several $1000 more than than a ICE that with my personal driving habits, I will almost never even need to stop at a charger outside of my residence ( a huge plus in my MN – I hate filling up for gas in bad, cold weather) which will be way less maintenance and much much lower fuel cost – sign me up, now. Now I tend to own cheap compact cars for long periods of time, no luxury sedans of SUVs, so it will be awhile for me to see an EV worth the investment – but it will come far sooner than your conservative analysis.

Also, so many multiple car families, where only one vehicle needs good long-range capabilities. So interest in EVs for say, at least 25% of households that have more than one vehicle, will come far sooner than complete range parity with ICE cars. Yes, this isn’t moment when every vehicle bought will be an EV, but it is huge driver for demand in near future

There are lots of good points there. The reason I am being super conservative using the ‘matching or exceeding’ condition is because Seba was claiming an almost total wipe out of ICE vehicles (which I arbitrarily defined as 95% to account for the fact that some people will hang on to ICE vehicles just like they hang on to mechanical watches as status symbols).

The autonomous vehicle and decline in car ownership question is something I have thought a lot about; to tell the truth, I am not sure which way it will swing so left it out. As I put in a reply to another comment, counter-intuitively cheap EVs that have autonomous functions may actually encourage car ownership. I know the dominant argument currently is that we will all switch to autonomous Uber-type transport solutions, but people love to own things, personalise them and display them. It goes back to the non-transport functions of cars; that is cars held for status signalling and aesthetic reasons.

Facebook is built on the fact that humans like to curate an image of themselves and then project that image to the outside world. In the process, they display ‘stuff’ and ‘experiences’ to the outside world. Cheap EVs that could have almost infinite form factors and can be kept anywhere (and summoned at will so no parking constraints) will be better expressions of identity than existing ICE vehicles. In short, how many people post photos of their Uber pick-up experience as opposed to their new Model 3?

And thinking about it, and it’s not a great thought given the climate change and other environmental implications that stem from it, but won’t EV ownership more likely follow the example of fast fashion? That is the same forces that have led us to triple the annual purchase of clothes over the last few decades will also be replicated with EVs (here I mean increase overall demand for vehicles not reduce it). Ultimately, EVs will be cheaper, more varied, and easier to maintain than ICE vehicles –and just like fashion you can order them online. Moreover, and this advantage exceeds fast fashion, they will be easier to store since you can tell your autonomous vehicle to go and find a parking space for the night even if you live in a tiny apartment with no allocated parking space. As an economist by training, I would say that all these factors would suggest greater vehicle ownership, not less. Not good I know.

First of all, excellent series of posts. One thing I was thinking the whole way through is that a key component to Seba’s prediction is the rise of autonomous vehicles, which is why in his presentation he said it wasn’t a one-to-one replacement. I agree most people won’t want to give up cars, but many will and it’s likely that many families will only need one car. If Uber only cost $1-2 per ride across town, it would have a tremendous impact on car ownership. So I guess I’m saying I’m doubtful we’re looking at 130M cars in 2030. I also think carmakers will be embarrassed to make ICE vehicles in a few years, similar to how many automakers are shifting away from diesel.

Hi Daniel. Yup, I am aware of the autonomous vehicle side to Seba’s argument. I don’t deal with it direct since a) there is no expert consensus on the speed of adoption of autonomous vehicles and, more importantly, b) I think autonomous vehicles could actually make car ownership more attractive, particularly in urban areas in developing countries. The text below is part of my reply to someone else who raised this issue:

“The autonomous vehicle and decline in car ownership question is something I have thought a lot about; to tell the truth, I am not sure which way it will swing so left it out. As I put in a reply to another comment, counter-intuitively cheap EVs that have autonomous functions may actually encourage car ownership. I know the dominant argument currently is that we will all switch to autonomous Uber-type transport solutions, but people love to own things, personalise them and display them. It goes back to the non-transport functions of cars; that is cars held for status signalling and aesthetic reasons.

Facebook is built on the fact that humans like to curate an image of themselves and then project that image to the outside world. In the process, they display ‘stuff’ and ‘experiences’ to the outside world. Cheap EVs that could have almost infinite form factors and can be kept anywhere (and summoned at will so no parking constraints) will be better expressions of identity than existing ICE vehicles. In short, how many people post photos of their Uber pick-up experience as opposed to their new Model 3?”

We could also see the Jevons Paradox kicking in with a vengeance here:

https://en.wikipedia.org/wiki/Jevons_paradox

EVs are more efficient than ICE vehicles and growing more efficient by the day. Also, ultimately, they are simpler to make and, as battery costs come down, they will fall far below equivalent ICE vehicles in price.

Ultimately, EVs could (ironically for an environmentally friendly good) pull a lot of people off public transport and into cars. Think of the reasons why people use public transport. I would say the major reasons are

1. Can’t afford a car

2. Have nowhere to park a car where you live

3. Have nowhere to park a car where you work

4. Want to use the commute time for non-driving purposes

5. For environmental reasons

The rise of autonomous vehicles offsets all five factors. The EVs of the future will be cheaper to buy and run. The cars will pick you up at home and drop you off at work and find somewhere to park in the meantime. You can read a book in your autonomous EV or catch up on your emails. And you are not polluting when you move about (at least in terms of physical emissions, though you could argue that congestion and use of land for roads is a form of public pollution).

In short, following Jevons, greater efficiency will stimulate greater demand.

Another thing that will impact ICE sales is replacement by other mobility tech that may not have even been invented yet or is just getting started.

I own an ebike that I use to commute 30 miles r.trip to my work about 50 percent of time (and I live in MN, so weather severely limits this). I am 50+ years old out of shape woman, but I love the ebike and have converted many other friends with just one ride on the thing.

Sure ebikes will never get near the market share as cars, but look at the Netherlands, Copehagen, and consider ebikes make hilly towns flat and as easy to bike thru as those places, and consider ebikes in most medium to high density towns take equal or less time to get places and consider what how popular biking seems to becoming with younger generation – the impact of ever cheaper, and ever better ebikes is a non-trivial thing.

And there are other types of new vehicles cheaper batteries and better computers are making possible that could be similar game changers in 12 years – such as Sea Bubbles EV boats that could make stable electric ferries a new commuter option.

Little EVs like scooters, electric skateboards, single wheel things, electric mini-cars, electric moped will all be nibbling away at ICE cars in a death of a thousand cuts.

And your thorough post didn’t even address fleet autonomous cheap electric vehicles, even just small shuttles running on very fixed limited routes, loops, could really eat away at individual ownership of cars.

I comment to the autonomous question:

Yes people likes to own things like cars, as a sign of status.

However what we own may quickly shift !

A good breed horse was status a bit more than a centry ago, together with a nice carriage, or actually many of each.

Once the car came along, cars quickly became the thing.

But before that status was expressed in other terms, so there is nothing really saying that we will not find other ways of expressing wealth and status if transportation becomes a non issue (I.e. everyone rides around in luxury cars to/from the job, although you cannot tell who really owns the vehicle).

But I’ll think we will soon see how these things pan out once AI driving level 4 and above becomes commercially available in cars…

Great series! Thanks for taking the time to lay this out.

I think Tony is right, though: autonomous miles driven – and therefore cars purchased – will dwarf the Swiss watch outliers clinging to their personal cars.

The idea that ownership of autonomous EVs will be in vogue ignores the economies of fleets. The cost savings of utilizing a robotaxi vs buying, charging, storing, insuring and maintaining your own private robotaxi – while small – will add up quickly. You simply cannot make up the difference when competing with a company that utilizes their cars a factor of 10 times more than you do. And I don’t think you will be able to hire your car out to offset your costs because the fleet owner will be able to undercut your rate with their economies of scale.

So when everyone on Facebook is showing pictures of their many vacations they have gone on and toys they have purchased with the money they’ve saved, your pictures of your Model 3 will quickly come up short.

And even though total miles driven will increase as the young, elderly, transit riders and poor utilize the robotaxis, the fleet operators will still need less than half the number of cars to cover that increase.