The frustration within the sustainability and resilience blogosphere is palpable. Oftentimes it is expressed in terms such as this: “Why even bother communicating with the mainstream, when the mainstream has no intention of listening?”

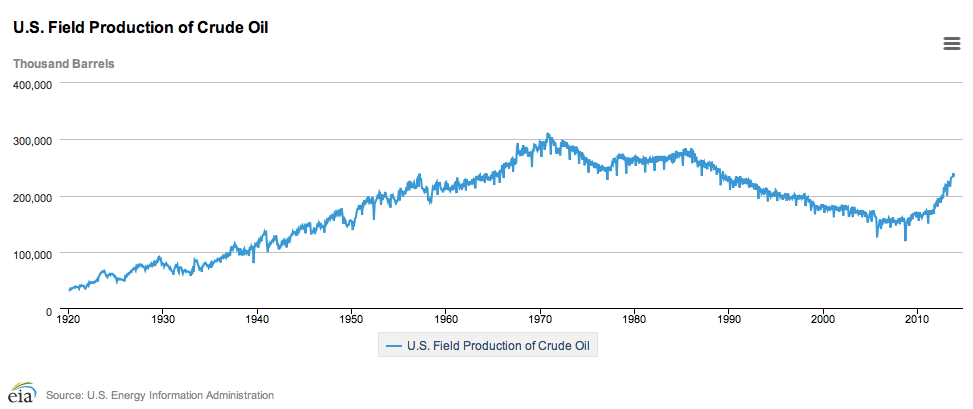

But ideas have a life of their own, and many are gradually infecting the mainstream, without the mainstream even being aware of their origin. For example, take the chart below titled “Costly Quest” taken from a Wall Street Journal article published on 28 January (behind paywall here, click for larger image):

This is a classic case of the Red Queen syndrome, under which Big Oil has to run ever faster purely in order to stand still; that is, ever more investment for the same level of production. (A previous post dealt with the Red Queen and shale gas here.)

The Red Queen can also be described another way: a decline in the energy return on investment (EROI), under which you have to put ever more energy into an extraction and production process just to get the same amount of energy out.

EROI was first conceived of by the systems ecologist Charles Hall who later developed it more deeply into the discipline called biophysical economics, the best exposition of which can be found in the book “Energy and the Wealth of Nations” by Hall and co-author Kent Klitgaard.

You can listen to a recent 19 January 2014 podcast by Hall talking about EROI and biophysical economics at Progressive Radio Network at the link below. Don’t get put off by the weird bird noises at the beginning. The podcast starts one minute in and Hall gets on to fossil fuel depletion issues about 25 minutes into the podcast. The first 25 minutes are still interesting as they explain how Hall got involved in biological energy systems when studying migrating salmon.

http://prn.fm/resistance-radio-charles-hall-011914-2/

At the height of the credit crisis, the revolutionary ideas espoused by advocates of biophysical economics chimed with the times and even got an airing in the mainstream media, as, for example, in this article in The New York Times in 2009.

Five years on and this intellectual strand of thought remains marginalised, as Joseph Tainter, one of the movements most high profile supporters predicted back then:

“Of course I’m trying to send a message,” said Joseph Tainter, chairman of Utah State University’s Department of Environment and Society. “I just don’t expect there’s anyone out there to receive it.”

And many who tried to get the message out have given up, the demise of The Oil Drum being, perhaps, the most famous example. Similarly, we got a post from the blogger Question Everything yesterday making a very definitive statement:

What follows is actually something that has been brewing for a while. I started writing this a little over a year ago. A recent e-mail list exchange with some other people who have been blogging, mostly about things like climate change, energy depletion, and the collapse of civilization, reminded me of my own evolution in thinking. Several well-known luminaries in the blog and book-writing world have begun to voice a kind of remorse that their voices have been ignored. Meanwhile the world has careened toward the consequences they have warned us of. And now they are realizing that they have been tilting at windmills. Somewhere along the line I did too…..

…..In any case I plan to no longer concern myself with warning of imminent collapse or a bottleneck. In all likelihood I may, from time to time, simply mention another signpost along the way, like the current draught problems in California as indications that climate change is having its effects much sooner than expected. But I won’t dwell on how it could have been different if only people would have listened to the warnings and taken heed. I won’t complain about those in governments being so incredibly stupid and foolish. I’ve said quite enough about it already. Think of this as a kind of retirement from the role of a Cassandra.

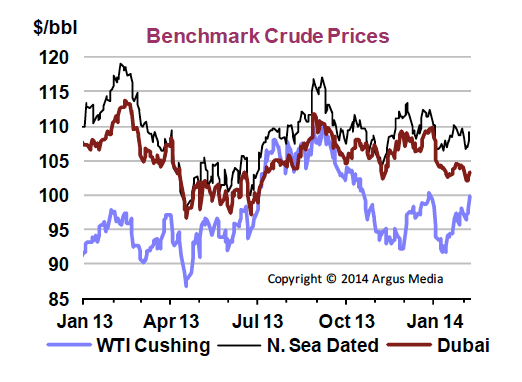

My own position is somewhat less gloomy. Why should we be so surprised that a well-financed climate skeptic lobby would have emerged after Al Gore’s “Inconvenient Truth” and the Intergovernmental Panel on Climate Change “Fourth Assessment Report” in 2007? Or surprised that, with an oil price spiralling above $100 per barrel, the fossil fuel industrial complex would throw more cash and technology at getting marginal barrels of oil out of the ground?

My optimism rests on the fact that our problems cannot be permanently ignored: the planet will continue to warm and energy prices will continue to rise. In The New York Times article back in 2009, Hall was quoted thus:

“It isn’t that there’s no technology,” Hall said. “The question is, technology is in a race with depletion, and that’s a whole different concept. And we think that we can show empirically that depletion is winning, because the energy return on investment keeps dropping for gas and oil.”

This is basically the core idea behind The Wall Street Journal article I commenced the post with.

So should we all give up? I think my answer is “no”: every idea has its time and biophysical economics is an idea whose time is just arriving. From the heretical to the mainstream in tiny incremental steps. Indeed, in the not too distant future, even The Wall Street Journal will believe in the idea of peak oil and dangerous anthropogenic climate change. You may call me stupid and naive; I prefer to see myself as patient.